Summary

- Production of natural gas liquids (NGLs) has grown over the past decade, and strong international demand has led to significant growth in exports.

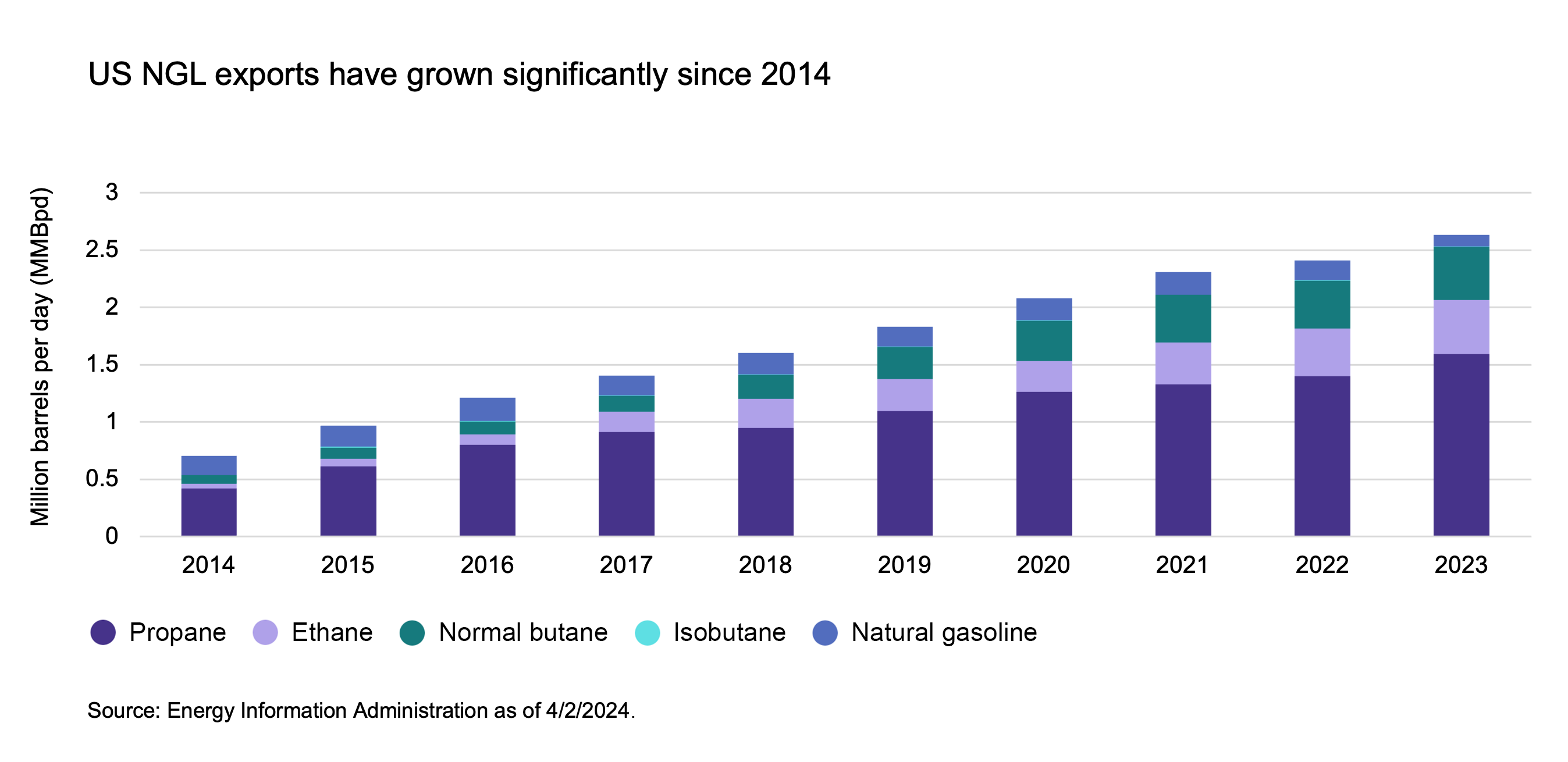

- Exports of NGLs grew by 274% over the past 10 years, with demand driven largely by the plastics manufacturing industry.

- Midstream companies continue to invest in NGL infrastructure from processing capacity to pipelines.

While propane and butane are relatively familiar natural gas liquids (NGLs) given their use in consumer cooking applications, much of the global demand for NGLs actually stems from plastics manufacturing. As demand for plastics around the world has grown, so has the demand for NGLs as feedstocks. Given strong international demand, exports of NGLs have been steadily growing, and midstream companies are investing across the NGL value chain. Today’s note looks at growing NGL exports and how the midstream space is investing in NGL-focused infrastructure.

US NGL Exports: A Decade of Growth

Natural gas liquids (NGLs) are produced from wells alongside oil and natural gas. Midstream companies with gathering and processing businesses collect the raw natural gas from well heads. They then separate NGLs and natural gas at gas processing plants. The NGLs then get separated into their respective components (propane, ethane, butane, isobutane, and natural gasoline) at fractionation facilities. And those are also typically owned by midstream companies.

Demand for NGLs, particularly propane and ethane, has been climbing for the past 10 years, largely driven by plastics manufacturing. Midstream companies have been building incremental fractionation and export capacity to meet growing demand (read more). For propane, exports make up most of the demand for US production, which has been rising steadily (read more). There has also been solid growth in ethane exports (read more).

Overall NGL exports rose 274% between 2014 and 2023, from 0.7 million barrels per day (MMBpd) to 2.6 MMBpd. The chart below depicts this. Looking ahead, exports are poised for continued growth with midstream companies currently building additional export capacity. The Energy Information Administration (EIA) expects modest NGL production growth in the U.S. in 2024 and 2025. Rising NGL production and exports continue to be a growth driver for the energy infrastructure space.

Midstream Companies Invest in NGL Infrastructure

Midstream MLPs and corporations participate across the NGL value chain, including Energy Transfer (ET), Enterprise Products Partners (EPD), MPLX (MPLX), ONEOK (OKE), and Targa Resources (TRGP). Beyond gathering and processing, companies are pursuing growth projects with pipelines, fractionation facilities, and export terminals.

Growing production of NGLs requires additional pipeline capacity from the Permian to fractionation facilities in Mont Belvieu, Texas. That is the Gulf Coast NGL hub. EPD is building the Bahia NGL pipeline, which will transport up to 0.6 MMBpd of NGLs from the Permian to EPD’s fractionation facilities in Texas and is expected to be in service in 1H25. TRGP is building the Daytona NGL Pipeline, which will run parallel to its Grand Prix Pipeline and connect NGLs from the Permian to Mont Belvieu. Daytona expects to be in service in 4Q24. OKE is also expanding its West Texas NGL Pipeline to Mont Belvieu, with the pipeline set to come online in 1Q25.

Expansions in the Works

An expansion is underway for the BANGL Pipeline, which transports NGLs from the Permian to the Gulf Coast and is a joint venture between WhiteWater Midstream, MPLX, WTG, and Rattler Midstream. The pipeline is being expanded by 75,000 barrels per day (Bpd), and 200,000 Bpd and is expected to be in service by 2025.

More production also requires more processing capacity. EPD, ET, TRGP, and OKE are all currently building new fractionators. EPD has the largest fractionation footprint on the Gulf Coast, with 1.67 MMBpd capacity in Texas and Louisiana. At Mont Belvieu, ET has 1.15 MMBpd of fractionation capacity, and TRGP has around 1.1 MMBpd of capacity. OKE has around 0.9 MMBpd capacity in total, with some of its fractionation capacity located in Kansas.

ET, EPD, and TRGP are the midstream companies with NGL export facilities. ET has over 1.1 MMBpd of NGL export capacity and is expanding its Nederland and Marcus Hook NGL export terminals, with expected completion in mid-2025. EPD loaded about 0.82 MMBpd of NGLs for export in 2023 at its Enterprise Hydrocarbons Terminal and Morgan’s Point Ethane Terminal. EPD is also developing the Neches River Ethane/Propane export facility expected to come online in 2025-2026. The facility will initially add 0.12 MMBpd of ethane export capacity. TRGP has export capacity of 13.5 million barrels per month (equates to about 0.45MMBpd).

Bottom Line:

NGL production and exports have grown significantly over the past decade. Midstream companies are investing in building additional infrastructure to meet growing production and rising demand, particularly from overseas.

Related Research:

Strong NGL Outlook Drives Midstream Growth

Propane Helps Fuel Midstream/MLP Growth

MLPs and the Fastest-Growing Hydrocarbon You’ve Not Heard Of

For more news, information, and strategy, visit the Energy Infrastructure Channel.