The Federal Reserve continues to hold fast to its highly data-driven, wait-and-see approach on rate policy. Last week’s FOMC meeting further bolstered the market’s belief in a lone rate-cut scenario, and senior loan ETFs have gained traction as elevated rate expectations spill over into the second half of the year.

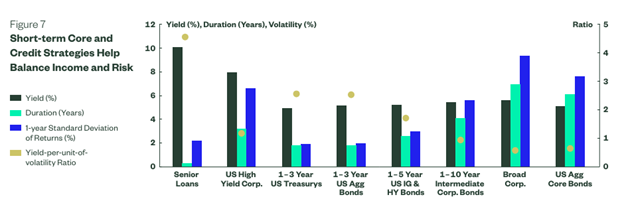

Despite record rate volatility, senior loan ETFs have risen above the fray and emerged as a beacon of resilience. They’ve captured the attention of investors scouring the credit quality spectrum for lower volatility and higher yield. Senior loans boast some of the healthiest carry in the debt space. Compared to junk bonds, which are yielding 8%, senior loans are spouting a historically high yield of above 9% — in some cases, nearing double-digit returns.

The additional 4% yield on top of Treasuries presents a tantalizing trade-off for those willing to take on more credit risk, given their below-investment-grade status. The floating-rate coupon also helps cushion the blow against rising rates and inflation. Consequently, senior loans tend to have less rate sensitivity than the broader bond market, preserving bond value and minimizing capital depreciation and income loss. They’re typically low duration — with interest payments widely resetting every 30 to 90 days.

Source: State Street Global Advisors

Strong institutional demand for senior loans, coupled with a strong economic backdrop, has driven credit spreads ever narrower. But tighter spreads can be justified by a stable, credit-friendly macroeconomic outlook and a steadily higher-for-longer rate environment. Additionally, the creditworthiness of senior loans not only benefit from their legal precedence over all other claims, but from a perceived tightening of bank lending standards over the past few years.

Pathway to Private Credit

The Invesco Senior Loan ETF (BKLN) stands out as the largest, oldest, and most liquid senior loan ETF. Now pacing for its seventh straight month of inflows, the $8 billion behemoth has taken in $870 million in May alone — and has accrued north of $2 billion in new money this year. The fund follows the Morningstar LSTA US Leveraged Loan 100 Index — focusing on a broad array of large senior secured loans and investing via a market-weighted “sampling” methodology.

Salman Zaidi, director of institutional specialties at Invesco, stressed BKLN’s role as a pivotal gauge for private credit markets.

“Senior loans have historically had a high correlation with private credit,” he said. “Given BKLN’s exchange-traded feature, it provides a convenient, transparent, public market instrument with a high correlation — over 0.8 over the last decade — to private credit. Sophisticated investors are increasingly looking at that high correlation, plus its low duration and daily intraday liquidity to utilize BLKN as a proxy for private credit.”

The shift toward ETFs for accessing private credit marks a departure from traditional avenues such as private equitylike funds, which lacked liquidity and tradability. Private credit is also filling a big void on the supply side of the loan business. Since last year’s regional banking crisis, many smaller banks have retreated from middle markets and pulled back from lending to smaller businesses.

Active Senior Loan ETFs: Steady Stream of Inflows

Investors can find another high income, low volatility option in the space with the SPDR Blackstone Senior Loan ETF (SRLN), which has seen $1.2 billion in net inflows this year. The $6.6 billion fund uses an actively managed floating-rate loan strategy and has amassed $630 million in net inflows in May, making it one of the most popular active ETFs of the month.

The Eaton Vance Floating-Rate ETF (EVLN), a relatively newer entrant that launched earlier this year, invests broadly across the floating-rate loan market. The fund is managed by Eaton Vance — a loan market pioneer since 1989 — and uses a time-tested, bottom-up approach to credit research and risk management. EVLN has been steadily gathering assets, enjoying $785 million in net inflows year to date. The ETF overall provides access to corporate term loans heavily weighted toward the software sector. It’s worth noting EVLN also charges less than many of its peers in the senior loan ETF space — just 0.6%.

Other active senior loan ETFS like the PIMCO Senior Loan Active ETF (LONZ) and BlackRock Floating Rate Loan ETF (BRLN) have also enjoyed positive net inflows for the year.

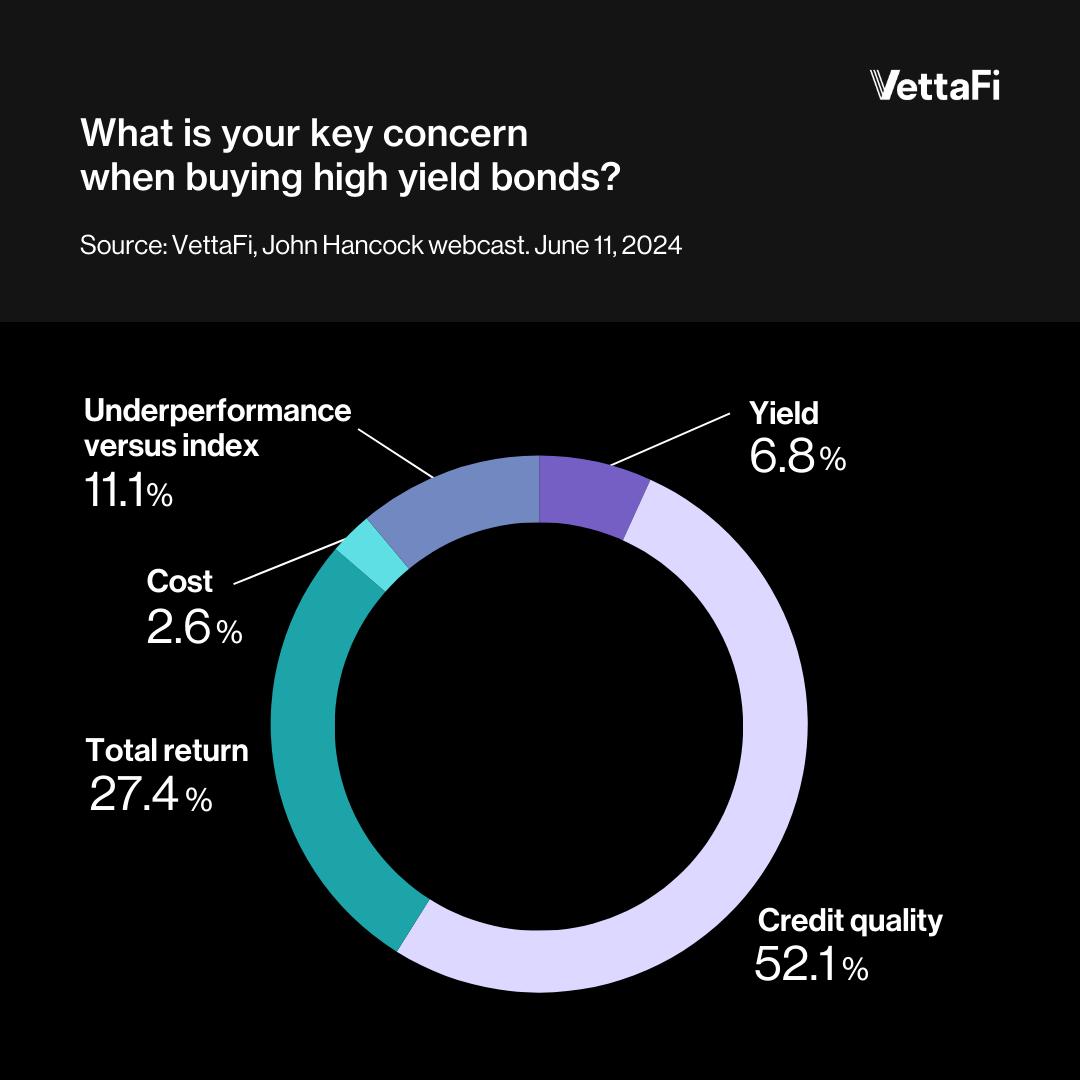

On a recent webcast, we asked advisors what their primary concern was when buying high yield bonds. More than half of them said credit quality, followed by total return. Arguably, senior loans can allay some of these key concerns.

Private credit and bank loans have become a crucial source of financing for corporate borrowers — and are playing an increasingly pivotal role in portfolio allocation, even for individual investors. The evolving landscape underscores the importance of innovative financial instruments like senior loan ETFs in providing both yield and stability amidst uncertain market dynamics.

For more news, information, and analysis, visit VettaFi | ETF Trends.