Critical materials are essential for clean energy applications and technologies like electric vehicles and wind turbines. This category includes copper, lithium, nickel, cobalt, and rare earth metals. However, the use of critical materials and rare earths goes beyond clean energy. These metals are also used in military equipment, medical devices, and essential technology applications.

On a regular basis, the United States, other countries like China and Australia, and governing boards like the European Commission publish a list of critical or strategic raw materials deemed economically and strategically important for the economy and have a high risk associated with a supply shortage. While the metals on these lists may differ slightly, the overarching concern is the same: economic and national security and stability. The lists are constantly evolving and changing as well. For example, the EU’s first list published in 2011 featured only 14 critical materials. The most recent list published in 2023 had 34 critical and strategic metals.

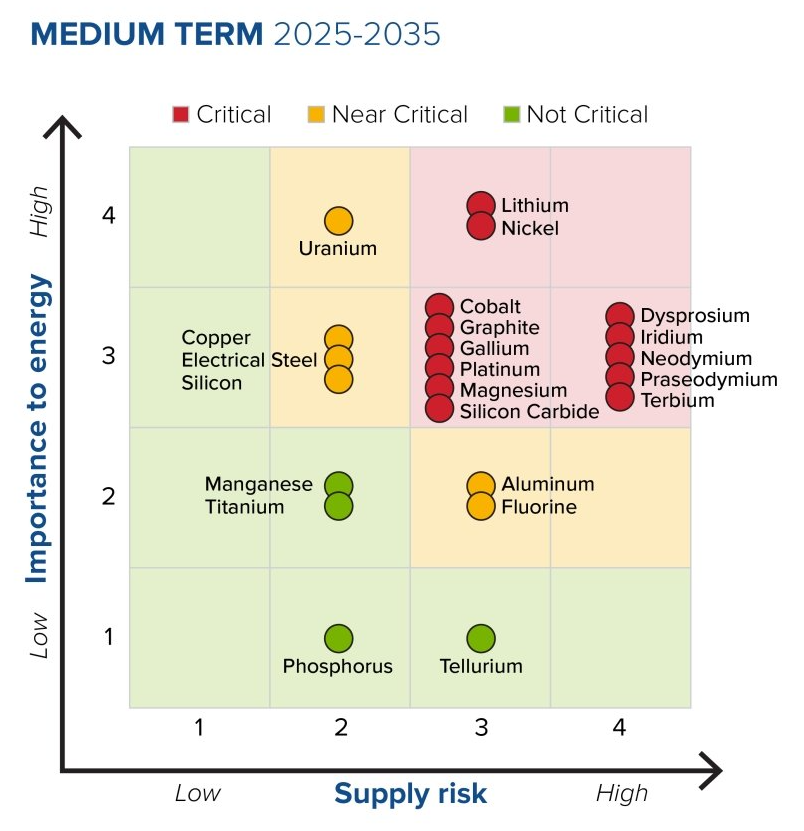

Below is a graphic depicting medium term supply and energy importance according to the US Department of Energy.

Source: Energy.gov

China Dominance

Of particular concern is the current global reliance on China for critical materials. The country not only has essentially complete control of the global refined stockpile of natural graphite, but it also controls the processing for 90% of manganese, 70% of cobalt, nearly 60% of lithium, and 40% of copper refining. Ironically, China dominates the processing of the world’s critical materials even as it remains the world’s largest source of greenhouse gas emissions.

Another critical material on these lists is uranium, which is essential for nuclear power and fuel production. According to the World Nuclear Association, China also targets producing one-third of its uranium within its borders.

The Covid era provided a rude awakening with regard to the global potential for supply chain disruption. As a result, countries are scrambling to build more resilient supply chains and secure domestic sources of critical materials. However, as with any commodity with high demand and limited supply, prices remain high, creating growth opportunities for companies producing these metals and materials.

ETF Plays for Rare Earths

Several ETFs provide investors with exposure to the rare earths and critical materials theme. The largest and oldest of these ETFs is the VanEck Rare Earth and Strategic Metals ETF (REMX). It has $337 million in assets and has been around since 2010. It is concentrated, with 33 holdings, and has a 24% weight to China. Its year-to-date performance has languished this year relative to its peers, and the fund is down 24.4%.

By contrast, its smaller competitor with $7.5 million in assets, the Optica Rare Earth & Critical Materials ETF (CRIT), which tracks a VettaFi index, is down only 0.74% for the year. The key difference might be related to its limited China exposure of only 11.3% and better diversification, holding 55 names.

Another ETF in this category to consider is the Sprott Energy Transition Materials ETF (SETM). It holds $16 million in assets and is down only 0.26% this year. It has very little exposure to China and is very diversified with over 100 holdings.

| Symbol | ETF Name | Total Assets | YTD |

| REMX | VanEck Rare Earth and Strategic Metals ETF | $336.8 | -24.42% |

| SETM | Sprott Energy Transition Materials ETF | $16.3 | -0.26% |

| CRIT | Optica Rare Earths & Critical Materials ETF | $7.6 | -0.74% |

This year, China’s exposure and diversification have been “critical” to the performance of these funds, and over the long term, as China’s critical metal dominance is challenged, that trend might continue.

For more news, information, and analysis, visit the Disruptive Technology Channel.