Summary

- Six constituents in the broad Alerian Midstream Energy Index (AMNA) spent a combined $1.49 billion on equity repurchases in 1Q24.

- Aggregate buyback spending among midstream/MLPs in 1Q24 was more than double the amount from 4Q23.

- Over 84% of constituents in AMNA by weighting currently have a buyback authorization in place.

With energy infrastructure companies generating significant free cash flow, buybacks have become an important avenue for shareholder returns in addition to growing dividends. Midstream buyback activity rebounded in 1Q24 even while most names saw strong performance during the quarter. Today’s note looks at 1Q24 repurchase activity and existing midstream buyback authorizations.

Midstream Buyback Activity Rebounded in 1Q24

For midstream, buybacks complement dividends to enhance total shareholder yields (read more). Six constituents of the Alerian Midstream Energy Index (AMNA) collectively repurchased $1.49 billion of common equity in 1Q241. While activity was concentrated around just six names, the aggregate spending on repurchases was more than double the level seen in 4Q23 (read more).

Cheniere Energy (LNG) has driven the bulk of midstream buyback activity and continued to lead the group in 1Q24. Cheniere spent $1.2 billion on buybacks in 1Q24, marking its most active quarter for repurchases yet as its shares came under pressure and management used the weakness as a buying opportunity. LNG shares fell from ~$170 at the start of the year to below $153 in mid-February. For context, Cheniere spent $339 million on repurchases in 4Q23 and nearly $1.5 billion on buybacks in all of 2023. As discussed on its May earnings call, management’s goal is to bring Cheniere’s common shares outstanding to 200 million from 229 million in late April. Cheniere has approximately $950 million remaining under its current share repurchase program and an upsized authorization is expected later this year.

Outside of Cheniere, buyback activity was generally conducted against a backdrop of strengthening equity prices. Targa Resources (TRGP) repurchased $124 million in equity during the quarter, the second-most of AMNA constituents, while its stock rose nearly 29%. TRGP paid a weighted average price of $104.26 per share in 1Q24 while the average price it paid for buybacks in all of 2023 was $76.72 per share.

In its first buyback since 2022, MPLX (MPLX) spent $75 million on repurchases in 1Q24. EnLink Midstream (ENLC) and Enterprise Products Partners (EPD) repurchased $50 million and $40 million in equity during 1Q24, respectively. These three companies also saw strong equity price performance during the quarter. Rounding out the group, Kinder Morgan (KMI) had a small repurchase of $7 million.

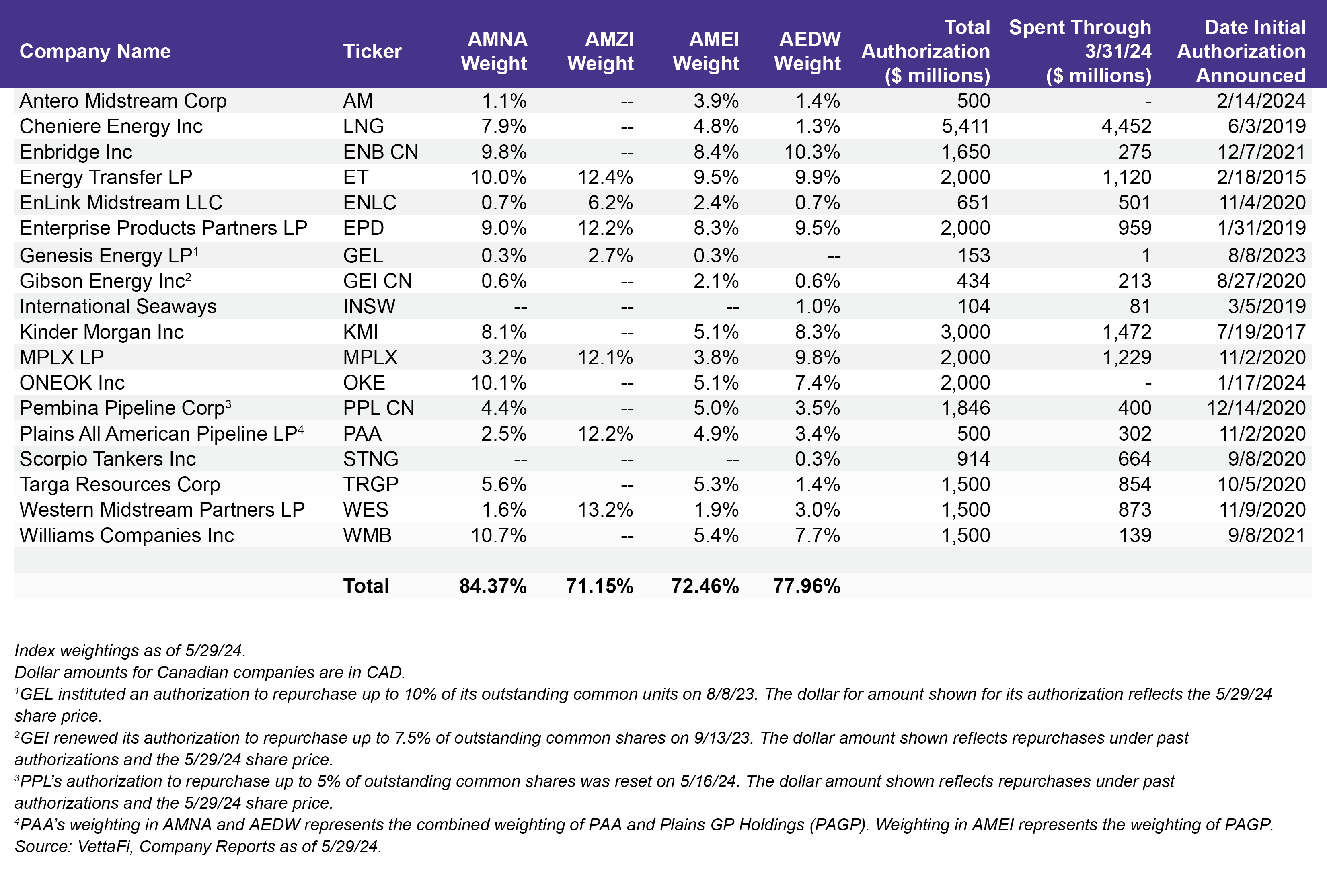

The table below shows the energy infrastructure companies with buyback authorizations in place, how much each has spent on repurchases, and each company’s weighting in AMNA, the Alerian MLP Infrastructure Index (AMZI), the Alerian Midstream Energy Select Index (AMEI), and the Alerian Midstream Energy Dividend Index (AEDW). More than 70% of the indexes by weighting as of May 29th have buyback authorizations in place.

Plenty of Dry Powder for Future Buybacks.

A handful of companies have renewed or initiatied a new buyback authorization this year. Alongside a dividend icnrease, ONEOK (OKE) announced a new $2 billion buyback authorization that is expected to be executed over four years. Antero Midstream (AM) introduced a $500 million authorization, while ENLC reauthorized its $200 million program, which it plans to complete. In May, Pembina Pipeline Company (PPL CN) renewed its buyback authorization for five percent of its outstanding common shares. While companies will evaluate buybacks against other uses of capital, names with new and existing authorizations have ample room to deploy excess cash flow if desired.

Bottom Line:

Midstream/MLP equity buybacks rebounded in 1Q24 as Cheniere significantly stepped up its activity and other names continued or resumed buybacks. Midstream names have ample dry powder for additional buybacks based on new and existing authorizations.

Related Research:

Examining MLP/Midstream Dividend and Buyback Yields

4Q23 Caps Solid Year for Midstream/MLP Buybacks

For more news, information, and analysis, visit the Energy Infrastructure Channel.

1 Aggregate dollar amounts include Canadian dollars for the Canadian corporations with repurchase programs.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AEDW is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP) and the ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND, for which it receives an index licensing fee. However, AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMNA, ENFR, ALEFX, MMLP, and AMND.