In the ever-evolving landscape of finance, understanding market dynamics is paramount. At Astoria, we continually monitor trends to inform our investment strategies and provide clients with solutions that meet their desired growth or income outcomes. Here are the key observations and strategies shaping our approach today.

The Return of Bad News as Good News

Amidst weaker economic data, such as disappointing NFP numbers and ISM falling into contraction territory, we witnessed yields fall, the probability of a rate cut increase, and stocks rally. This underscores a shift in sentiment where bad news is once again being interpreted as good news, at least in the context of monetary policy and market performance.

Equities and Yield Dynamics

Equities are in a delicate phase of the cycle. While the economy exhibits signs of weakening, the prospect of imminent Fed rate cuts remains distant. Additionally, despite being solid, earnings aren’t being rewarded as much as in previous quarters. Moreover, valuations for market-cap-weighted indices are stretched. Equities are hungry for lower yields to attract holders of T-bills, CDs, and money market funds into the stock market—a delicate balance to maintain.

Bonds Facing Challenges

Bonds were anticipated to shine in 2024, with seven rate cuts priced in and inflation seemingly tamed; however, reality tells a different story. Bonds are having a rough year, with the AGG down 2% as of Friday, May 3, 2024.

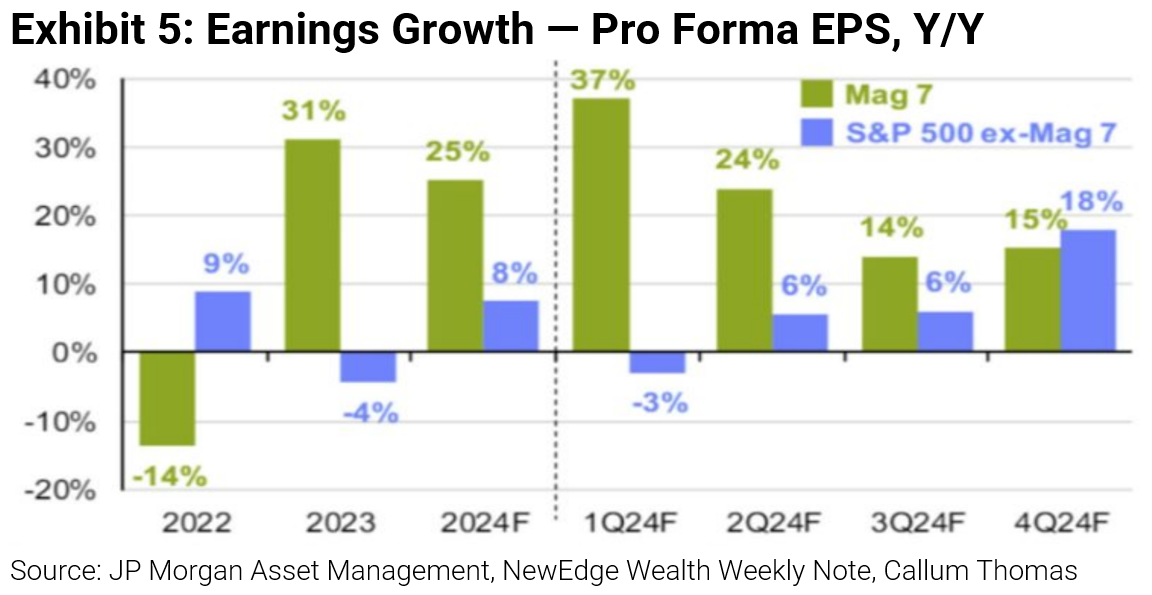

Tech, Inflation, and Alternative Assets

Tech stocks continue to play a crucial role in portfolios, with expectations of driving significant earnings growth in the coming years. Astoria does not think it is wise to bet against tech, but we encourage investors to be diversified; in this spirit, Astoria implements an equal-weight strategy that mines the highest quality large and mid-cap stocks, sector-optimized so as not to bet against tech or any other sector for that matter. Meanwhile, inflation remains a concern, impacting various asset classes differently. Gold, for instance, has seen a bid, which can be attributed to money printing, widening deficits, and increased economic volatility.

Market Overview and Astoria’s Approach

Despite short-term headwinds, the market presents a generally favorable setup for the average stock, particularly outside the mega-cap realm. Astoria advocates allocating to a broad, diversified basket of US and international equities with tilts toward inflation-sensitive assets.

Astoria’s ETF Model Portfolios

In response to evolving market conditions, Astoria has adjusted its ETF model portfolios in 2024. This includes sticking with quality exposure (QUAL, QGRO, DGRW, etc.); we diversify our equity exposure with approximately 1/3 equal-weight, 1/3 market-cap-weight, and 1/3 smart beta.

-

QGRO is one of the few quality growth ETFs in the market that diversifies away from Mag 7 risk. +32% in 2023; +7% YTD. With this quality growth ETF, you don’t get the massive concentration risk presented by market-cap-weighted ETFs tilted toward the Mag 7. The largest weight is Booking Holdings at 3.2%. MSFT is at 3%, and Google is only a 2.7% weight.

-

We continue to advocate for Japan (DXJ) for its combination of strong earnings estimate revisions, high growth estimates, strong price momentum, and relative cheapness (13.6x P/E). Japan’s GDP has room to grow, and corporate finances have improved: companies have more equity than debt.

-

Within fixed income, we are barbelling between corporates, Munis, and Treasurys. We are net neutral duration. We also started buying Mortgage-backed bonds (SPMB). Agency MBS have higher spreads than corporates, attractive YTMs, and low prepayment risk.

-

We reduced negatively correlated alts like BTAL.

-

Astoria remains bullish on real assets, such as our inflation-sensitive real assets strategy and gold (GLDM).

The Role of Quantitative Selection and the Quality Factor

Over time, the Equal Weight S&P 500 Index has outperformed the Market Cap-Weighted S&P 500. From Jan. 1999 through Dec. 2023, the SPXEW has cumulatively outperformed SPX by 310%. Past performance is not necessarily indicative of future results. See chart below.

Astoria’s use of quantitative stock selection pervades our strategies. We’ve seen our inflation-sensitive strategy serve as a beneficiary for earnings revisions. A recent Morgan Stanley research report highlighted that the strongest revisions breadth in the past four weeks is from Telecom, Diversified Financials, Materials, banks, Autos, and Energy.

Source: Morgan Stanley Research.

Notable ETF Trends and Looking Ahead

-

Bitcoin gets all of the headlines, but there are more timely diversification strategies you can implement in the short term, such as adding equal weight to market cap-heavy portfolios, diversifying into select International Markets, and incorporating real assets into traditional stock and bond portfolios.

-

Equal weight serves as a complement to large-cap growth and blend strategies. As mentioned, Astoria approaches equity diversification with 1/3 equal weight, 1/3 market cap weight, and 1/3 smart beta.

-

Don’t expect investors to trickle out of T-Bills and money markets into corporate bonds and spread products unless rates fall to 3-3.5%.

-

Fixed income has taken in $72 bln, which is 30% of the total ETF inflows YTD; a surprising stat given AGG is -2% YTD vs. SPY +8%.

-

2024 ETF flows will depend on the economic data and Fed cuts.

-

Small-caps / Value needs to see rate cuts for performance to catch up with SPY.

-

Russell 2000 index +1% YTD

-

S&P 500 Value Index +4% YTD

-

-

EM is starting to turn the corner with the recent bid in Chinese equities and the slowdown in US economic data. KWEB +13% and MSCI Emerging Markets Index +6% YTD.

Warranties & Disclaimers

As of May 3, 2024, Astoria Portfolio Advisors held positions in AGG, QGRO, QUAL, DGRW, DXJ, SPMB, SPY, BTAL, and GLDM on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.

Any third-party websites provided on www.astoriaadvisors.com are strictly for informational purposes and for convenience. These third-party websites are publicly available and do not belong to Astoria Portfolio Advisors LLC. We do not administer the content or control it. We cannot be held liable for the accuracy, time-sensitive nature, or viability of any information shown on these sites. The material in these links is not intended to be relied upon as a forecast or investment advice by Astoria Portfolio Advisors LLC, and does not constitute a recommendation, offer, or solicitation for any security or any investment strategy. The appearance of such third-party material on our website does not imply our endorsement of the third-party website. We are not responsible for your use of the linked site or its content. Once you leave Astoria Portfolio Advisors LLC’s website, you will be subject to the terms of use and privacy policies of the third-party website. Refer here for more details.

Cover Photo Source: CNBC