We are in unprecedented economic times as global central banks try to offset the inflationary impacts of record amounts of economic stimulus enacted to offset the economic effects of the COVID-19 pandemic. Uncertainty is further increased given the importance of the coming elections not just in the U.S., but globally as well. Globally, more voters than ever will head to the polls as at least 65 countries, representing 49% of the world’s population, are set to hold national elections this year. These elections will reflect and impact an increasingly uncertain geopolitical and global economic environment.

Despite these uncertainties, the underlying fundamentals of the U.S. private sector, including households and businesses, is on solid footing though not without risks that are worth considering. For example, though loan delinquencies have been rising, they remain at historically low rates both as a percentage of loans outstanding as well as in terms of dollar amount of loans outstanding.

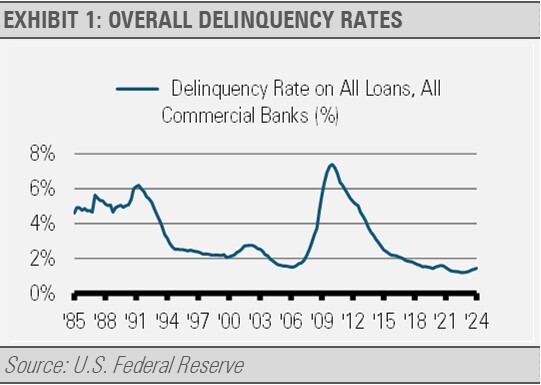

As the following exhibit shows, the delinquency rate on all loans at U.S. commercial banks is roughly 1.5%, far below the norms of recent decades including the strong economic years of the 1980s and 1990s.

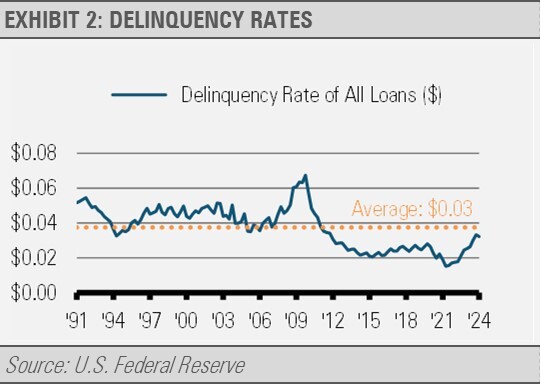

Looking deeper, for every dollar of outstanding consumer loans and leases, just over 3% or $0.03 is delinquent. This rate has increased from its recent all-time low but is still well below the average for the last three decades.

We are seeing delinquency rates increase in credit cards and auto loans most specifically, while government intervention may be keeping student loan delinquency rates depressed. These delinquencies may primarily be related to the drawdown in savings of the bottom quintile of income earners. We have mentioned this risk previously and will continue to track it closely for signs of possible contagion.

Meanwhile, corporate net worth is near an all-time high. Businesses have plenty of cash on hand to fund further investments in plants and equipment as well as research and development.

This store of cash does not include their ability to tap the financial markets for financing, which is the more traditional way that firms fund growth. Continued investment can lead to stronger future economic growth and productivity gains.

INVESTMENT IMPLICATIONS

Given the global uncertainties and the soundness of the U.S. private sector, we think that a focus on quality equities and high-quality fixed income investments in the belly of the yield curve offer the best risk-adjusted potential. By doing so, investors can be shielded from global uncertainties and benefit from the strength of U.S. corporate balance sheets and the potential for further economic growth.

We favor businesses with persistent and strong profits as well as limited debt-to-equity, especially the leading businesses in technology, financial services, and healthcare.

By investing in quality, investors may benefit from this persistent growth, which should translate into earnings growth, while also potentially providing protection should the economic situation deteriorate more than expected. We continue to increase our emphasis on these areas as we see substantial return potential for disciplined investors.

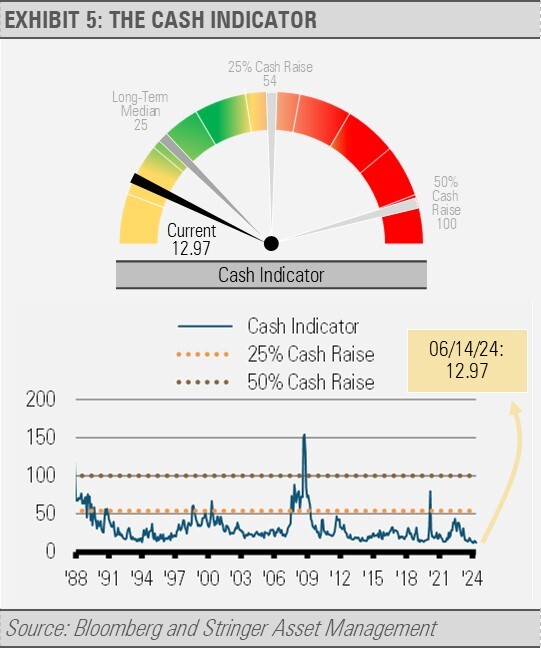

CASH INDICATOR

The Cash Indicator continues to meander near historic lows. We think that the excessive amount of cash in the global financial system is among the contributors to such persistently low market volatility. Given the solid economic backdrop, we think that investors should be prepared to take advantage of the opportunities to purchase high quality assets at discounted prices as volatility reemerges.

For more news, information, and analysis, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.