Mixed economic data throughout May continued to befuddle investors looking to capitalize on near-term interest-rate cuts. The odds for a summertime reduction in the Fed Funds rate appear remote now, and the possibility for no rate cuts in 2024 remains real. The U.S. economy continues to grow, albeit at a more moderate pace, while inflationary pressures remain somewhat sticky.

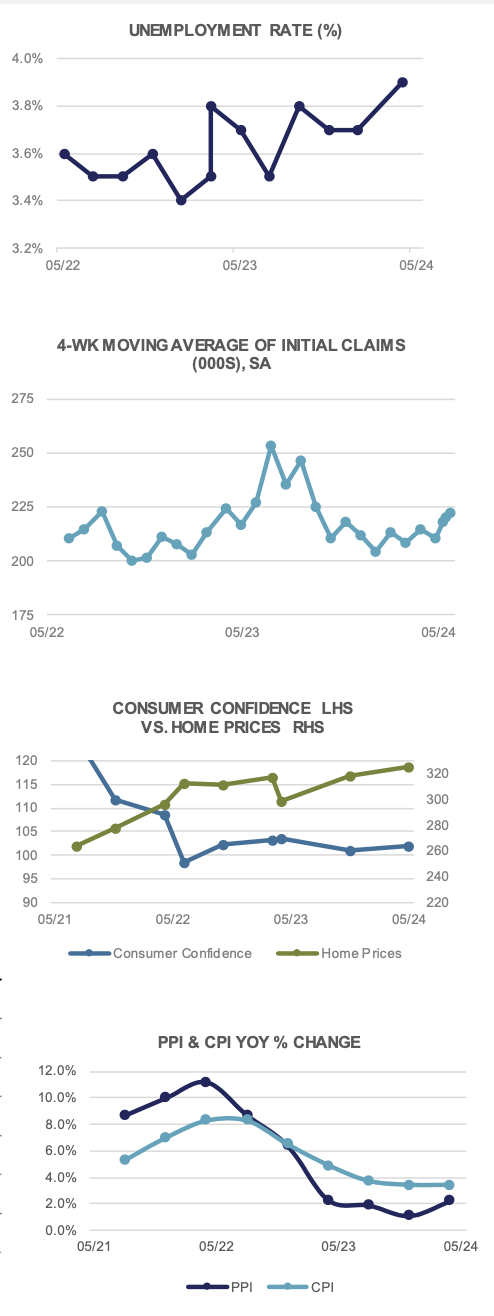

Unemployment in the U.S. is still sub-4% (April = 3.9%) while the JOLTS (Job Openings) number for March was 8.5 million. Moreover, wage pressures continue with Average Hourly Earnings up +0.2% MoM (+3.9% YoY) in April. Initial Jobless Claims have yet to move materially higher, averaging 219k for the month of May.

Consumer Prices edged up +0.3% in April, which translates to a +3.4% rise YoY, measurably higher than the Fed’s stated goal of 2.0% inflation. Core CPI also rose +0.3% MoM, and is now up +3.6% YoY. Producer Prices rose a higher than expected +0.5% on the month, but are only up 2.2% YoY (Core PPI was +0.5% MoM and +2.4% YoY). Consistent with these moves, the PCE Deflator rose +0.3% in April, and is now up +2.7% YoY. All in all, inflationary pressures have abated from the 2023 highs, yet remain above the Fed’s goal of 2.0%.

The University of Michigan Sentiment index dipped unexpectedly in May, falling from 77.2 to 67.4, while the U. of Michigan 1yr Inflation expectations survey came in higher than forecast at 3.5%. The longer-term 5-10yr inflation expectations forecast also came in a little higher than anticipated at 3.1%, suggesting consumers expect future inflation to come in markedly higher than over the prior decade.

The U.S Federal Reserve remains caught in a political pickle, with a reasonably strong U.S. economy, somewhat restrictive monetary policy currently, inflation still above target, and a U.S. election coming in November. Cutting interest rates will be an increasingly popular campaign slogan as we move through summer, with incumbents everywhere looking for an economic tailwind to carry them through to re-election. The Fed’s independent status may be sorely tested as Chair Powell surveys the economic landscape over the quarters ahead. Our guess remains 50/50 that we see an interest rate cut here in 2024, unless we experience a substantial slowdown in the months ahead.

DOMESTIC EQUITY

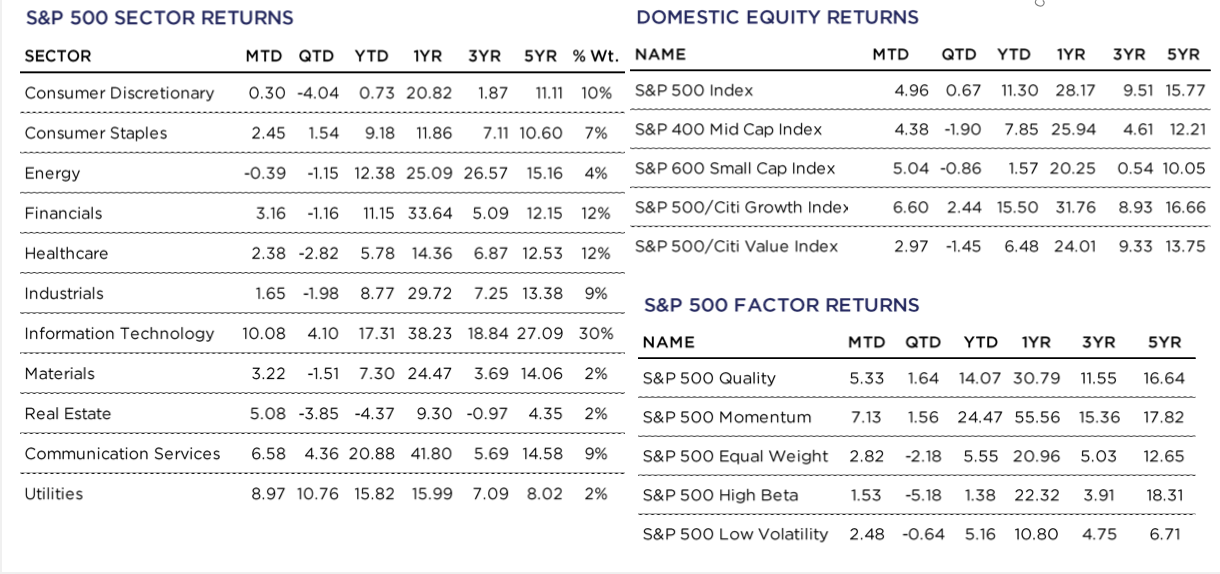

All three major US indices finished May in the black, notching their sixth positive month in seven. The top performing indices, led by the NADAQ, increased +6.9%, the S&P 500 gained +5.0%, and the Dow Jones added +2.3% during the month. Every sector in the S&P 500 finished May with gains, except for Energy. The largest gains during the month came from Information Technology, Utilities, and Communication Services rising +10.1%, +9.0%, and 6.6%, respectively.

Utilities have been a notable winner not only in May but throughout the year, posting gains of +15.8% YTD, outpacing all but two sectors in the S&P 500. Utility companies stand to benefit from the Artificial Intelligence (AI) boom as energy dependent data centers are needed to power AI. According to a recent Citibank report, data centers could account for 10.9% of US electricity demand by 2030, up from 4.5% today.

Shifting to technology, Nvidia posted earnings earlier in the month and beat Wall Street’s already lofty expectations. Nvidia has been a key benefactor riding on AI tail winds. The chips that Nvidia produces are essential for artificial intelligence platforms and are in high demand. Nvidia CFO, Colette Kress has stated demand for Nvidia chips will outpace supply well into 2025. Sales were up 262% in the first fiscal quarter and earnings were up 461% from a year earlier. Meanwhile guidance into the next quarter exceeded analyst estimates. This helped result in a +26.9% gain in the month of May, putting Nvidia’s YTD returns at +121.4% at the time of this publication. Nvidia stated they will also be issuing a 10-for-1 stock split, making the over $1,000 stock more accessible to retail investors. We will be watching to see if Nvidia can continue its strong performance.

Small-caps and Mid-caps (SMID) also rallied during the month. The S&P 600 and S&P 400 were up 5.0% and 4.4%, respectively in May. Price to earnings ratios remain below their 10-year average in the SMID space as elevated interest rates have kept valuations lower, although the gap was reduced after a positive month in May.

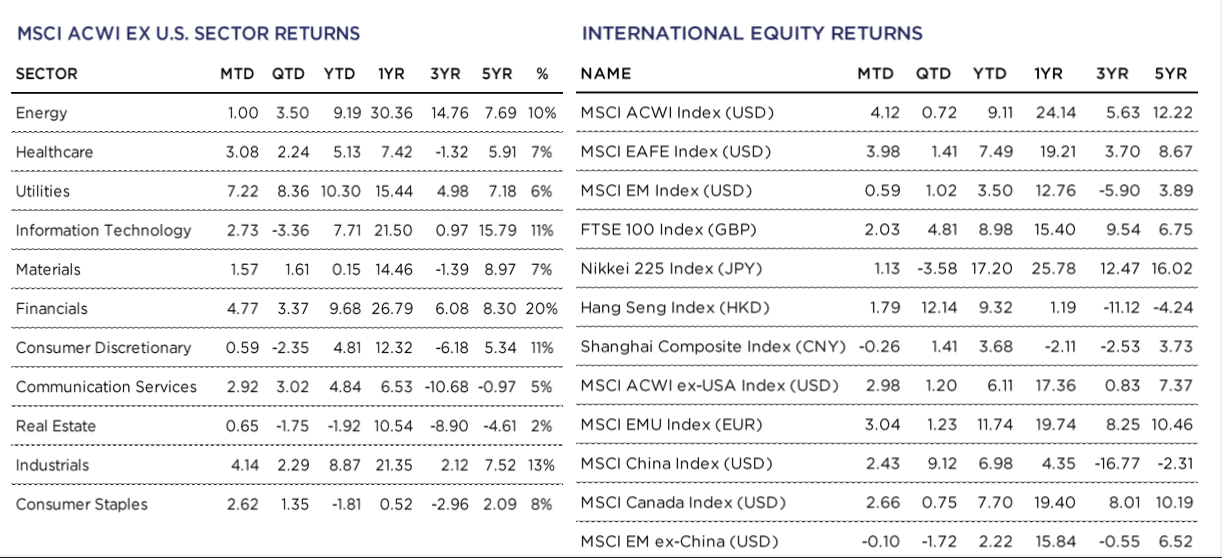

INTERNATIONAL EQUITY

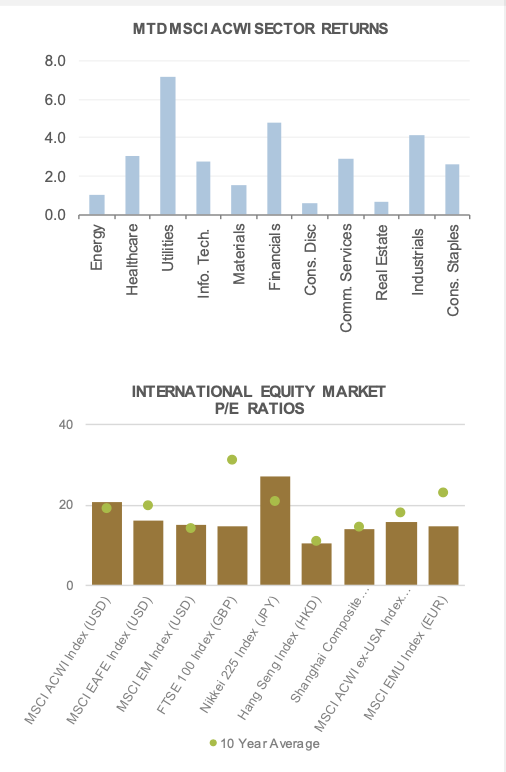

International equities reversed course during the month of May with the MSCI ACWI ex-USA Index returning +3.0% (in USD). Developed Markets (DM), as measured by the MSCI EAFE Index, gained +4.0% while Emerging Markets (EM), as measured by the MSCI EM Index, returned +0.6% (both in USD).

Strong performance was felt in Europe as many market participants anticipate the European Central Bank will cut interest rates for the first time since 2019 at their meeting on June 6th. Although European inflation has neared the bank’s 2% target, it rose more than expected in May and remains sticky in the European services sector. Regardless, many ECB decision makers have recently made public comments sharing their support in moving forward with this first 25bp cut, bringing the ECB’s deposit rate down to 3.75% from 4%. There is much less certainty, however, in the path of interest rate cuts for the remainder of the year, with markets now expecting two interest rate cuts, down from three when the ECB met in April and the expected five from the January meeting. The MSCI EMU Index returned +3.0% over the month and now boasts an +11.7% return YTD (EUR).

Chinese investors enjoyed positive performance during the month of May, which came as a bit of a surprise as the official manufacturing purchasing managers index (PMI) fell to 49.5, down from 50.4 in April. Readings below 50 indicate contractionary levels in the manufacturing sector. Nonmanufacturing PMI (measures construction and services activity) fell to 51.1, down from 51.2 in April. Though not a large decrease, the May reading did come in below expectations. Although the PMI numbers came in softer than expected, the International Monetary Fund (IMF) upgraded it’s 2024 economic growth forecast in China to 5%, up from the 4.6% level back in April. Over the month, the MSCI China index gained +2.4% and has returned +7.0% YTD, a number many did not expect following the start to the year that China had (USD).

All eleven of the MSCI ACWI ex-US Sectors posted positive returns in May. Utilities (+7.2%), Financials (+4.8%), Industrials (+4.1%) and Tech (+2.7%) all led the way, while Consumer Discretionary (+0.6%) and Real Estate (+0.7%) lagged behind.

FIXED INCOME

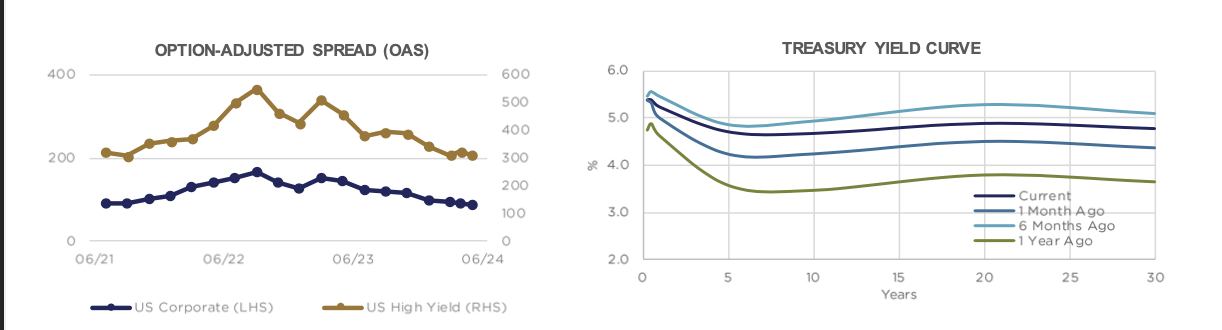

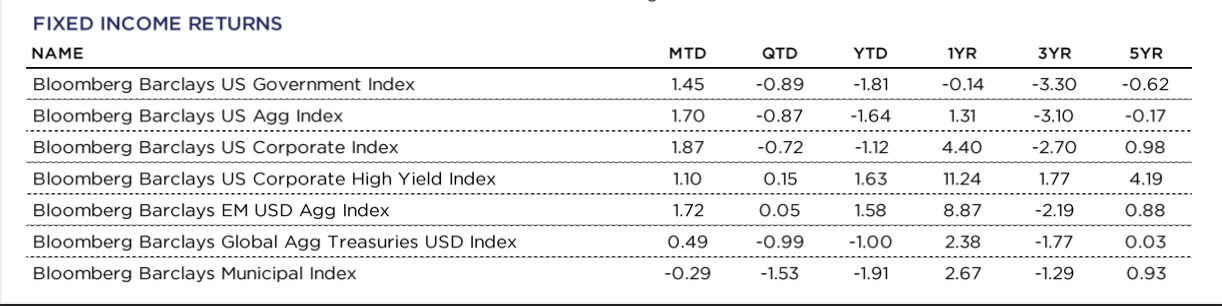

Interest rates moved lower across the Treasury yield curve during the month of May, with the twenty year maturity decreasing by the greatest margin, roughly 23 basis points. This movement in rates provided a tailwind to fixed income performance, leading to broadly positive returns from bonds, with the exception of tax-free municipal bonds. Yields remain significantly higher than where they began the year, as the markets (and the Fed) wait for inflation data to become more accommodating to the potential for any rate cuts.

The US Government and Aggregate indices produced monthly return of +1.4% and +1.7%, respectively. The Aggregate index’s performance benefitted from having exposure to the Investment Grade corporate bond market, which was the top performing category in May.

Investment Grade bonds led the way with a monthly return closing in on two percent. This return was driven by the decline in interest rates pushing bond prices higher, some credit spread tightening also pushing prices higher, and an appealing yield topping up the total return to a very attractive level for May.

High Yield bonds also benefitted from declining yields pushing prices higher. This benefit was counterbalanced by some spread widening leading prices lower. The yield produced gave High Yield a total return of just over one percent, significantly trailing Investment Grade bonds in May. Even with this month’s underperformance, High Yield is still the top performing category YTD.

The negative return experienced by municipal bonds in May can be explained by a significant cheapening of 5 year, 7 year, and 10 year maturities. These were the most expensive portions of the municipal bond market, and this month’s valuation adjustment brought these tenors back in line with more traditional levels relative to Treasury bond yields.

ALTERNATIVE INVESTMENTS

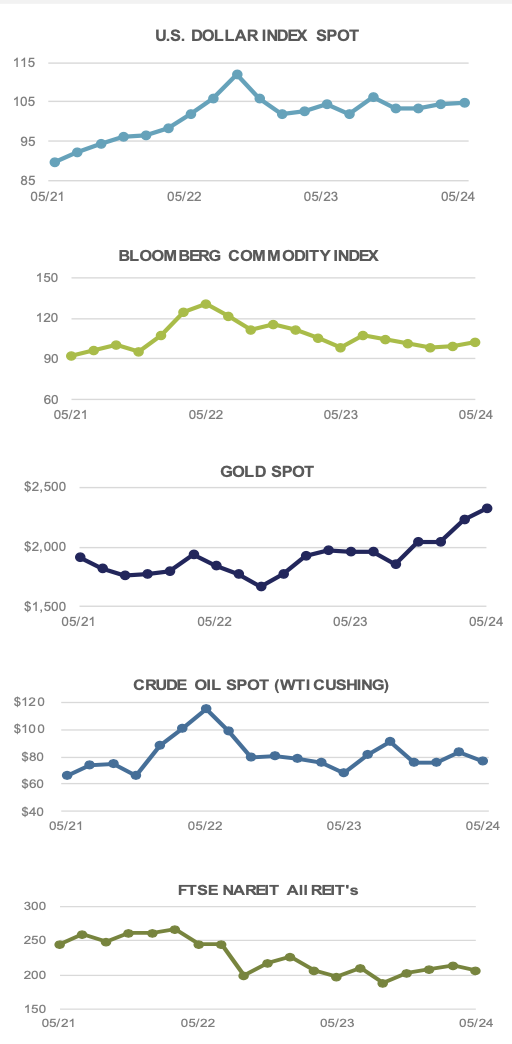

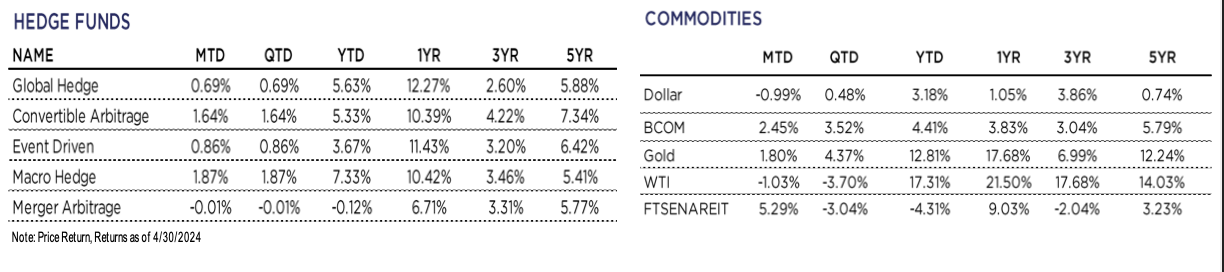

Alternative Investments had mixed results in May. Broad commodities, as measured by the Bloomberg Commodity Index, gained +2.5% for the month, boosted by a weaker U.S. Dollar as the DXY Index dropped -1.0%. Gold remains a top performing asset, returning +1.8% for May and +12.8% YTD.

May saw continued consolidation in the Oil & Gas sector with ConocoPhillips announcing a $22.5 billion dollar all stock deal to acquire Marathon Oil. This comes on the back of ExxonMobil closing its $68 billion-dollar deal to buy Pioneer Natural Resources, and a shareholder approval of Chevron’s near $60 billion-dollar proposed buyout of Hess. Expanding land rights in lucrative regions like the Permian Basin in Texas and the Bakken formation in North Dakota is a driver of deal activity.

As we go to press, OPEC+, the group of large oil producing nations, agreed to extend production cuts into 2025. With the IEA forecasting oil demand to grow by an additional 1.1 million barrels per day this year, the impact of production cuts on prices will be something to watch closely.

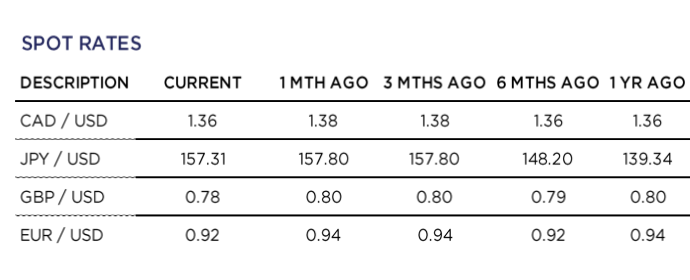

Making headlines in currency markets, the Japanese Government confirmed it had been intervening to prop-up the Yen; spending 9.8 trillion JPY ($62 billion USD) from late April through the end of May after the currency fell to a 30-year low. The large differential in interest rates between the U.S. and Japan has led to a weaker Yen in recent months. Japan has ample reserves of dollar-denominated assets, giving them room to intervene further.

For more news, information, and analysis, visit the ETF Strategist Channel.