June is a key month for markets as nearly all the world’s major central banks are slated to meet and determine their policy stance and make any changes to interest rate policy and asset purchase programs. Outside of the Bank of Japan, the policy stance of the world’s major central banks has turned in a dovish direction, with the ECB slated to cut rates as soon as this month. To a US fixed income investor, global central bank actions are crucial to US rates and markets due to their impact on exchange rates, capital flows, and global economic conditions. The interconnected nature of the global economy means that policies set by central banks around the world can significantly influence US financial conditions, economic performance, and investor behavior. Here are the key central bank dates for this month and the probability of policy rate shifts as implied by interest rates markets.

June 5th – Bank of Canada (67% chance of an interest rate cut)

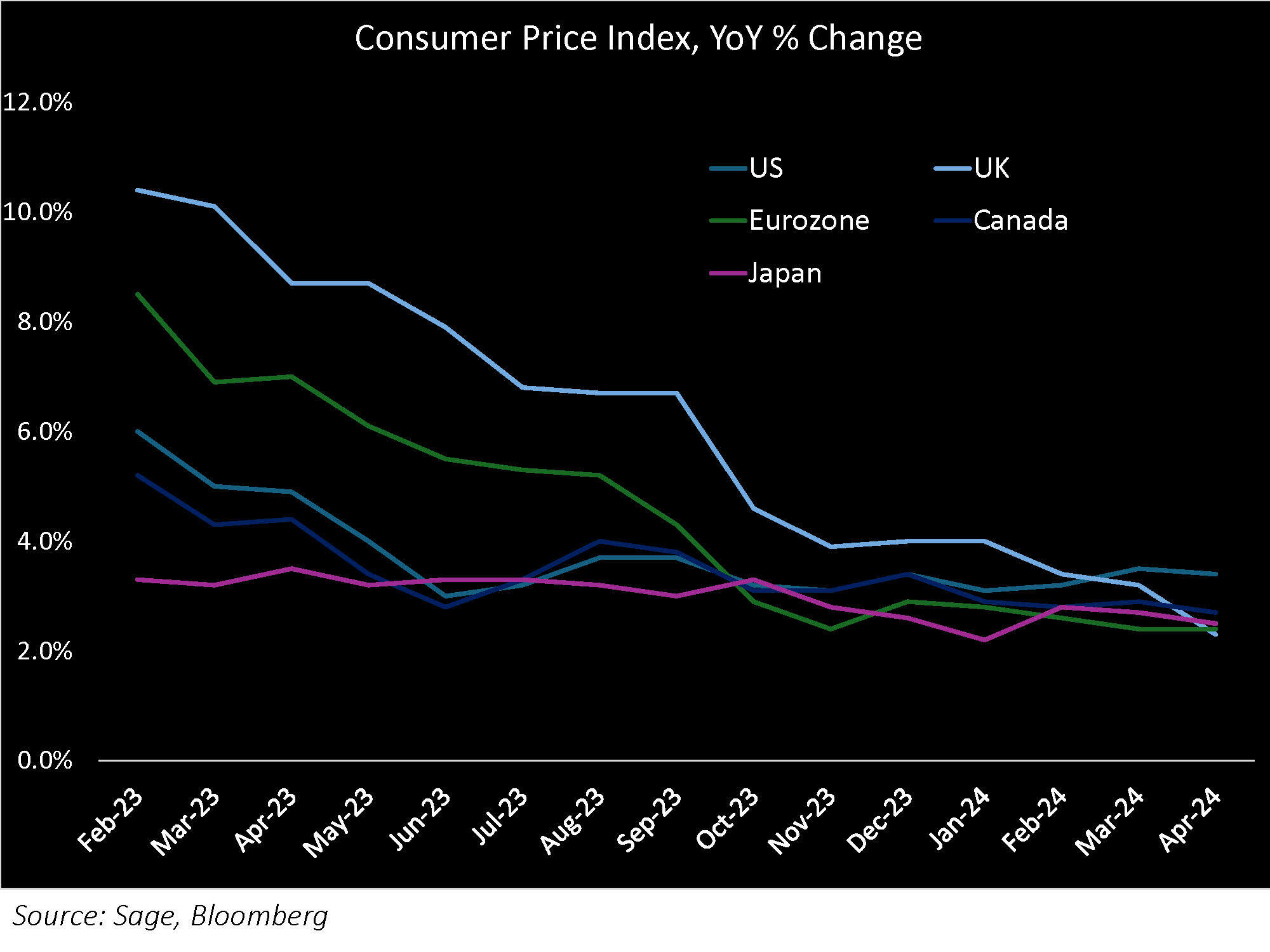

Canada CPI has been declining steadily this year, while growth readings remain below the strong US economic expansion, as Canada GDP registered a 0.6% growth at its most recent release on May 31st. Given its benign growth and inflation picture, the Bank of Canada is expected to start cutting interest rates as soon as its June meeting.

June 6th – European Central Bank (98% chance of an interest rate cut)

Given the Eurozone’s disinflationary trend coupled with its languishing economic growth, the ECB has communicated its intention to commence interest rate cuts at its June meeting as it aims to bring down borrowing costs.

June 12th – US Federal Reserve (2% chance of an interest rate cut)

Unlike economic conditions in Canada and the Eurozone, the policy picture remains muddled in the US. Above-trend inflation is at odds with the Fed’s intention to lower interest rates over time to bring its policy rate closer to its neutral rate of 2.5%. While we do not expect any policy changes during its June meeting, the Fed’s quarterly Summary of Economic Projections, Dot Plot, and Powell’s remarks during his customary press conference will further illuminate the Fed’s policy stance. We continue to believe that the FOMC is determined to cut rates in the face of weaker data and has largely ruled out rate hikes, which continue to present an asymmetric outcome to lower rates.

June 14th – Bank of Japan (26% chance of an interest rate hike)

The BOJ is the lone major central bank that is expected to tighten its policy stance and raise interest rates this year. While it is not expected to act in raising its policy rate during the June meeting, the BOJ could strongly indicate an impending rate hike in July. As a percentage of GDP, Japan is the most indebted major economy in the world by a wide margin, so the BOJ will have to take special care to raise interest rates amid extreme interest rate volatility, as markets have pushed the yen to its weakest level in four decades.

June 20th – Bank of England (6% chance of an interest rate cut)

While the Bank of England has indicated that interest rates are in restrictive territory, it is not expected to lower them in June due to strong services inflation releases in April. Like the Fed, the BOE is keen to cut rates if inflation moderates over the coming months.

If all goes according to market pricing, all else equal, we don’t expect a huge move in markets. All eyes continue to be on inflation data, which will determine the timeline for ECB and FOMC rate cut decisions.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.