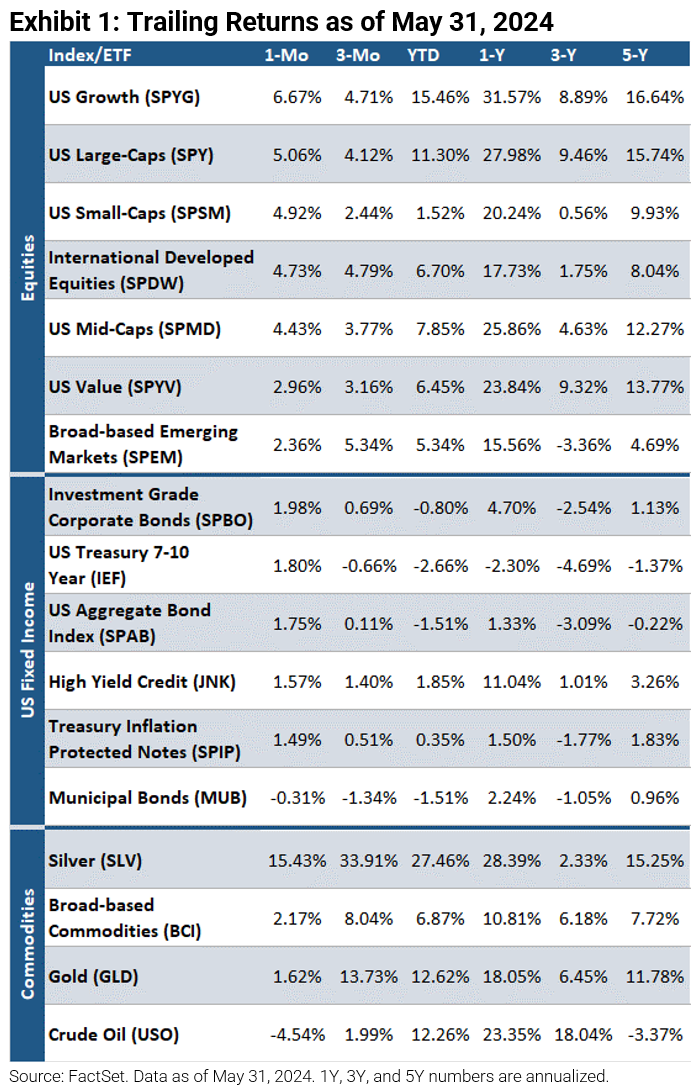

Major Indices Post Gains in May

Despite weakness in the last week of the month, all three major stock market indices were up in May amid strong earnings results and slightly cooler inflation. The S&P 500 posted its largest monthly gain since February (+5.0%) while the Nasdaq Composite had its best month since November 2023 (+7.0%). US growth (+6.7%) was among the best performers, followed by US large-caps (+5.1%) and US small-caps (+4.9%). Aside from munis (-0.3%), bonds were also up as investment grade corporates rose 2.0%, 7-10 year US Treasuries increased 1.8%, and the US Aggregate Bond Index gained 1.8%. Though crude oil was down 4.5%, commodities fared well as silver was up 15.4%, broad-based commodities rose 2.2%, and gold increased 1.6%.

FOMC Minutes Lean Hawkish

The Federal Reserve kept interest rates unchanged at the May FOMC meeting, leaving the fed funds rate at the 5.25–5.50% range. Although Fed Chairman Jerome Powell downplayed the idea of additional rate increases after the meeting, the FOMC minutes released on May 22nd leaned more hawkish. The report revealed various officials are willing to hike rates further if risks materialize, and that several policymakers expressed “uncertainty about the degree of restrictiveness.” The minutes also indicated that in the beginning months of 2024, inflation made less progress than policymakers anticipated. The Consumer Price Index (CPI) and Personal Consumption Expenditure (PCE) reports showed inflation eased slightly in April, but both core annualized measures remain stubborn and above the Fed’s 2% target (3.6% and 2.8%, respectively). Currently, investors are pricing in a 56% chance for the first rate cut to occur in September per the CME FedWatch Tool.

Is the US Economy Cooling, or Will it Strengthen Ahead?

The second preliminary GDP print for Q1 2024 came in at 1.3%, below both the estimate and first preliminary reading of 1.6%. This, along with cooling consumer spending from the April PCE report, a flat month-over-month April Retail Sales reading, and homebuilder sentiment unexpectedly turning negative via the May NAHB Housing Market Index release (see Exhibit 2), all support a cooling US economy.

A Strong Q1 2024 Earnings Season

Opportunities Outside the Magnificent Seven

The S&P 500 Posted Strong Gains YTD as Stocks Delivered on Earnings. We Remain Bullish

We acknowledge that the S&P 500’s rally in the first five months of this year (+11.3% YTD through May 31st) has been strong. Nevertheless, we remain constructive on equities.

We believe the overall S&P 500 isn’t nearly as attractive as the S&P 493 or even the rest of the world, which both present an abundance of opportunities. To be clear, we are still very constructive on stocks, but more so in non-Magnificent Seven names, US mid-caps, natural resources, commodity equities, precious metals, and non-US markets, particularly Japan.

Prudent in our methodology, our US large-cap portfolio construction includes equal-weighted exposures. If one only owns US large-cap market-cap-weighted products, their portfolio will have a relatively expensive valuation. However, if investors incorporate equal-weighted strategies, valuations can be lowered by approximately five turns or so.

For more news, information, and analysis, visit the ETF Strategist Channel.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, JNK, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, BCI, TLT, and LQD on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.