Thought to ponder…

“Adversity, illness, and death are real and inevitable. We choose whether to add to these unavoidable facts of life with the suffering we create in our own minds and hearts, the chosen suffering. The more we make a different choice, to heal our own suffering, the more we can turn to others and help to address their suffering with the laughter-filled, tear-stained eyes of the heart. And the more we turn away from our self-regard to wipe the tears from the eyes of another, the more— incredibly—we are able to bear, to heal, and to transcend our own suffering. This was their true secret to joy.

— Dalai Lama, Desmond Tutu, and Douglas Carlton Abrams The Book of Joy

The View from 30,000 feet

Last week was another week of records for the major equity indices, with the S&P500 breaking to new highs and the Dow Jones Industrial Average (does anyone follow the Dow anymore?) breaching 40,000, bringing back memories of the David Elias classic book “Dow 40,000”, where he speculated that the index would punch through that number by 2016. New equity highs were tied to two important economic releases, each of which broke in Powell’s direction, pushing interest rates lower, and inducing the upward action Pavlovian Response of the equity markets to lower rates. The initial driver of last week’s equity rally was a cooler than expected CPI release. It wasn’t so much that inflation was put on ice as it was a relief that inflationary momentum of the first three months of the year seemed to subside. The other big factor was Retail Sales, which took nosedive, dovetailing with the recently released blog from San Francisco Fed, which calculated that excess savings from the pandemic is officially exhausted, and data released from the New York Fed that consumer debt and delinquencies indicated further consumer strain. The combination of the perception of softer inflation with consumption headwinds fed a narrative that the economy would slow enough to support rate cuts sooner rather than later. Although, the recent run higher in equity prices supports our bullish call on equities, we caution not to get overly enthusiastic about a week or two of data. We believe the path for inflation, rates and consequently the equity markets, will be contingent on three forces – Labor Markets, Housing and Energy – each of which have been showing signs of weakness in the last month. If weakness persists in these areas, the Fed will likely embark on a mild rate cutting cycle this year, or perhaps a more aggressive campaign, if weakness shows signs of snowballing. Although rate cuts could ultimately bring positive outcomes for equities, the path higher for equities could be riddled with significant volatility if growth expectations erode along the way.

- Earnings Dashboard: Faceoff between Fab 5 Healthcare

- Housing holds the keys – higher active listings and falling sales may be signaling a shift in trend

- A downshift in Retail Sales links up with San Francisco Fed’s end of pandemic savings call and NY Fed delinquencies data

- Some of the other major stories of the week that have long-term implications: Emerging Markets and AI

- Focus Point Sector Rotation Update: Upward trends rocking and rolling everywhere but Energy and Consumer Discretionary

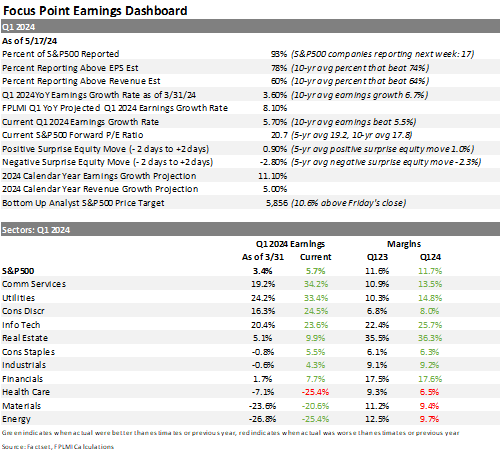

Earnings Dashboard: Faceoff between Fab 5 vs. Healthcare

- With earnings season nearly at the finish line, Q1 showed pervasive strength across all sectors except Health Care.

- More impressive than the earnings strength was the margin expansion, with consistency across all sectors except Health Care and all things pulled out of the ground.

- The most interesting thing about this earnings season was the continuation of the strength of the Fab 5 (Nvidia, Alphabet, Microsoft, Meta, Amazon) versus the weakness in Health Care led by the Terrible 3, Bristol Myers Squibb, Gilead and Data from Factset indicated that as of 5/10:

- Without the Fab 5 the S&P500 aggregate earnings would drop from 4% to -2.4%.

- Without the Terrible 3 the S&P500 aggregate earnings would rise from 5.4% to 9.7%.

- The coming week brings the grand finale of the earnings season when Nvidia reports on the 22nd. As with all grand finales, expect fireworks.

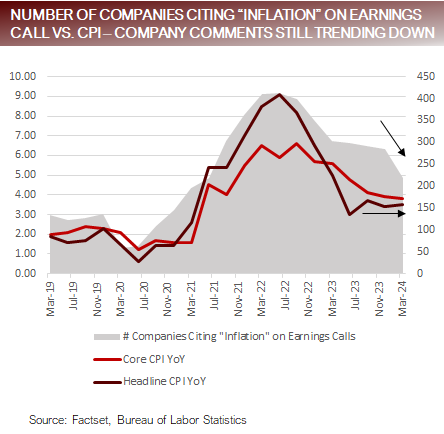

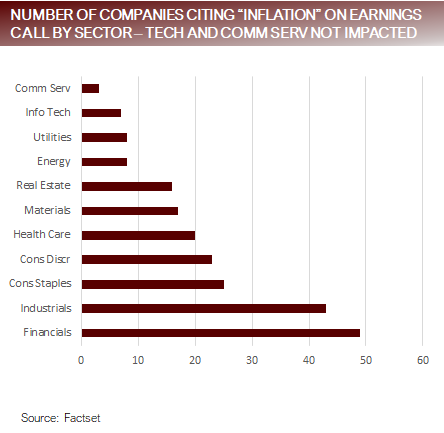

Companies have been citing inflation on earnings calls at a lower rate in 2024

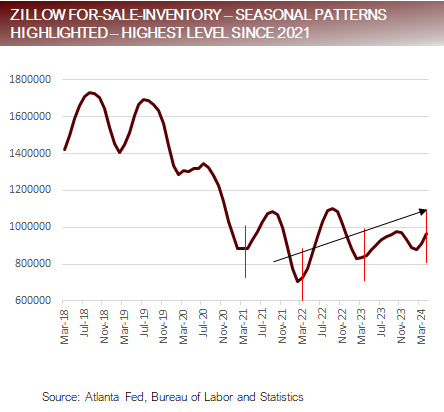

Housing holds the keys – higher active listings and falling sales may be signaling a shift in trend

- We’re following key trends in the housing industry which may be foreshadowing price weakness. According to Redfin as of 5/12:

- Active Listings New Listing (4-week rolling average)

- Active Listings were 890,224, up +14.2% YoY, and the highest over the last four

- New Listings were 102,269, up +10.0 YoY, barely the second highest over the last four

- Higher growth in Listings New Listings suggests inventory taking longer to clear.

- Active Listings has been showing a strong recovery and is now only about 18% lower than the average of the last three years prior to the pandemic, after dropping by as much as 50% in 2022.

- Pending Sales (4-week rolling average)

- Last week were 90,457, down -4.3% YoY, and the lowest level over the last four years

- Listing Price Drops (4-week rolling average)

- 6.3% of homes had price drops, the highest level over the last four years, and nearly 3x levels in 2021 and 2022.

- Redfin Homebuyer Demand Index

- Latest reading was 47, down -13% YoY, the lowest level over the last four years, and nearly 40% lower than 2021 and 2022.

- Active Listings New Listing (4-week rolling average)

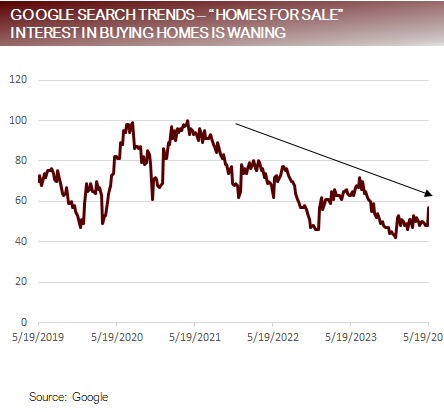

Interest in buying homes is waning while inventory swelling, signaling prices may move lower

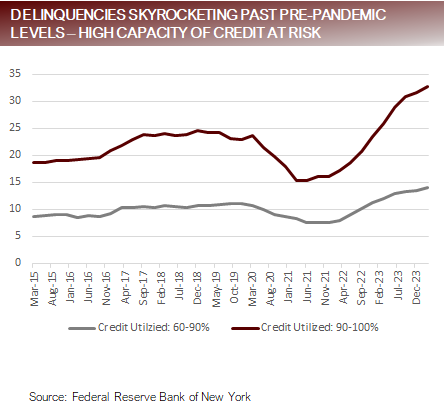

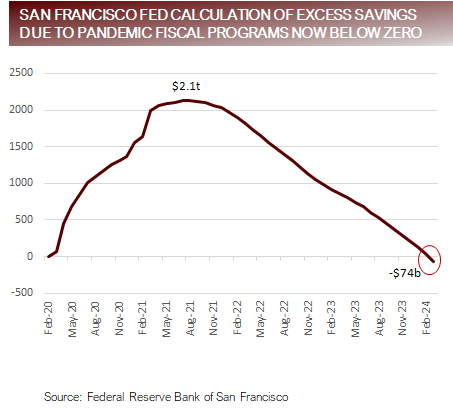

A downshift in Retail Sales links up with San Francisco Fed’s end of pandemic savings / delinquencies

- Advanced Retail Sales surprised to the downside, printing a month-over-month gain of 0% vs. consensus expectations of 0.4%, with a negative revision to the prior month. The Control Group, which excludes key components that add volatility, such as autos, building materials, office supplies mobile homes and tobacco, and is also used as an input for GDP calculations, missed positive expectations of 0.1%, printing -0.3%, with the previous month revised lower.

- The San Francisco Fed updated their research on pandemic level savings, which they estimated swelled to $2.1t, off the back of government sponsored programs, and has now reached -$74b, after falling every month since the middle of 2021, indicating consumers now have less on their balance sheets than prior to the The authors suggest that for consumer spending to be sustained, consumers will need to tap “less liquid” resources of debt to support consumption.

- Last week the New York Fed’s Center for Microeconomic Data released the Quarterly Report on Household Debt and Credit for the first quarter of 2024 which indicated consumers who utilize their available credit at a rate of 60% or higher have delinquency rates that have skyrocketed past pre-pandemic levels, with a third of consumers who are utilizing over 90% of their credit capacity transitioning into delinquency.

The extinguishing of excess savings is manifesting in higher delinquencies

Some of the other major stories of the week long-term implications: Emerging Markets and AI

- With economic and earnings data in the driver’s seat for most of recent market action, it’s tempting to have a myopic view and not see the big picture of some of the major themes unfolding in the world. There were some other significant topics crossing the tape last week that will likely have lasting impact on the financial markets, including:

- China committing $42b of State funds to buy unsold The program also included provisions to ease mortgage rules and extension of financing to state-owned enterprises. Although the program has been criticized as not a big enough canon, it’s a signal that Chinese authorities are attempting to put a floor under the markets.

- The prospect of rate cuts in the S. is boosting Emerging Markets, who have had to keep rates artificially high to keep their currencies from weakening against the USD. The pressure on Emerging Market Central banks to keep rates higher appears to be easing opening the door for lower rates in their economies as well. The effect of this is apparent when looking at U.S. equity performance versus Emerging Market equity performance. The S&P500 was up 1.54% last week, while the MSCI Emerging Market Index was up 2.63%.

- Recent AI releases have included Google’s Project Astra and OpenAI GPT-4o. The software advancements contained in these upgrades were significant and included the ability to engage in story telling and provide feedback without being prompted, as well of a host of other capabilities that up make AI seem more and more human.

- An article in the Wall Street Journal last week highlighted the impacts of falling fertility and shrinking population trends. This has long-term implication for GDP because as the population grows so does demand for goods and services, and vice-versa. To some degree productivity can make up for falling population sizes and sustain GDP, but ultimately falling populations will create headwinds for GDP

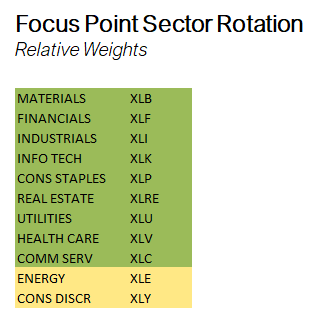

Focus Point Sector Rotation Update: Upward trends ex-Energy and Consumer Discretionary

- The Focus Point Sector Rotation Model is a combined trend following and mean reversion model that utilizes seven factors to analyze daily price data on sectors to determine the strength of upward trends.

- The S&P has been up for four consecutive weeks, driving every sector in the S&P500 over their 50, 100 and 200-day moving averages. However, even with the recent strength, the average sector is only 9% above the 50-day moving average, which indicates with a bad week or two the internal picture could change rapidly.

- The strongest upward trends are in Utilities, Health Care and

- Energy is teetering on moving to into a positive

Putting it all together

- On balance, economic data is coming in weaker than The Citigroup Economic Surprise Index, which measures data across the fully array of government data releases, comparing actual data published versus consensus estimates, is sitting at -23.2, the lowest level since May of 2022. For a refresher, the S&P500 was down about -18% for the year in mid- May of 2022, versus today when it’s up about +11%. The difference? The poor data versus estimates today is being viewed as ammunition for the Fed to cut rates.

- For the time being bad news is good That will change if the bad news begins to eat away to growth expectations. However, rounding the corner into the end of Q1 earnings season, estimates for the S&P500 for the full year are rising, margins are expanding, and extreme negative surprises have been isolated to a select number of companies within the Health Care Sector. As a result, growth is not being questioned, and the markets are being lulled into complacency by a lullaby of soft-landing music, which isn’t necessarily a bad thing, if that’s the outcome.

- We continue to have a positive view on the environment for risk assets, but weakening trends in the labor markets and signs of diminished pandemic bolstered saving and rising delinquencies are potential precursors to softening in consumer spending. If these trends were to continue, eventually it would trickle through to earnings and begin to dim the At the same time there is trend appearing for higher home inventories and a dimming of demand for homes, which Zillow is forecasting will push prices lower in 2025. These variables combined, could present a headwind to our positive outlook if they continue to develop unabated. However, we think ultimately, interest rate cuts are likely to cauterize the negative trends before they bleed into the economy and create significant damage.

For more news, information, and strategy, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.