Thought to ponder…

“Persistent and consistent effort over time can yield results. “So far” and “not yet” are the foundation of every successful journey.”

— Seth Godin, “The Practice”

The View from 30,000 feet

The highlight of last week was a showdown between two of the major forces in the markets: AI Earnings vs. Economic Data. Thursday last week had all the hallmarks of a Las Vegas title fight between the two heavyweight contenders. The fight got off to a vicious start as Nvidia stormed out of their corner in the first round with a flurry of jabs, brandishing an earnings release showing year-over-year quarterly revenue up 265%, with data center revenue up 409%. Their early move sent the stock from $950 to $1,033, generating follow-through in the markets as the S&P500 surged from 5,307 at the previous day’s close to an opening print of 5,341. It looked like Nvidia had a solid lead.

Then, Economic Data lumbered into the center of the ring and unloaded a powerful left hook, S&P Global PMI data, which came in stronger than expected. The Economic Data connected with the chin of the markets and buckled its knees. Within minutes, expectations for rate cuts fell and the 10-year Treasury spiked from 4.42 to 4.49, sending stocks into the danger zone. By the end of the day the S&P500 had collapsed from a high of 5,341 to close at 5,267. Economic Data had won the fight, highlighting an important lesson – AI Earnings matter, but Economic Data is running the show. This is an especially poignant lesson because last week also marked the end of Q1 earnings season releases, so all will be quiet on the earnings front for another six weeks with Economic Data being the only game in town. Given the propensity for Economic Data to land hard blows, it’s likely the next six weeks will provide some volatility. For their, part the Fed is engaged in theatrics around the ring by employing a barbell approach to messaging, where Powell gets out in front of audiences and provides market support with dovish comments, and the rest of Fed Presidents engage on an endless roadshow of speeches with hawkish comments. Last week’s Fed Minutes provided a classic example of the strategy as the dovish Powell press conference was juxtaposed against the hawkish meeting minutes. The Fed is attempting to carefully guide the markets to a soft-landing, using barbell messaging as a tool to buffer volatility that could otherwise threaten financial stability and create the need for more extreme measures of intervention.

- A Memorial Day message about the cost of war

- Krugman (Nobel laureate) “fanatically confused” about the next direction for interest rates

- Deciphering the good news is bad news effect

- Inflations expectations, inflation and political affiliations

- Focus Point Sector Rotation Update: Market pressure shakes off weak trends

A Memorial Day message about the cost of war

- There are a lot of ways to measure the cost of war. The most personal way is in lives. As we reflect on Memorial Day and remember the lives of the people lost defending our country, it’s helpful to provide some context of the volume of lives it has cost defending the United States (dead and wounded):

- American Revolution: 75,000

- Civil War: 1,129,000

- World War I 320,000

- World War II 1,076,000

- Korea 140,000

- Vietnam 212,000

- Afghanistan 22,000

- Iraq 37,000

- These numbers are both staggering, heartbreaking and a constant reminder of the cost of war.

- For the first time in decades Europe is engaged in struggles for sovereignty manifesting in drawn out war. According to the latest data published Ukraine and Russia have each lost as many as 500,000 soldiers, with tens of thousands of civilian Ukrainian casualties.

Krugman: (Nobel laureate) “fanatically confused” about the next direction for interest rates

- An interesting interview caught our attention last week by Bloomberg Television’s Wall Street Week, when David Westin interviewed Nobel laureate Paul Krugman. In the interview Krugman said he was “fanatically confused” about the next direction of interest Krugman identified what many on Wall Street and Main Street feel, splitting views into two camps:

- Interest rates are going higher for longer, with the neutral rates potentially moving higher

- Interest rates will settle back down to pre-pandemic and long-term trends

- There is evidence that the Fed is beginning to buy into the higher for longer and a higher neutral rate camp, demonstrated by the most recent Fed’s last Summary of Economic Projections, where the inched long-term interest rate expectations higher. It was only a marginal notch up from 5% to 2.6%, but it’s momentum in the upward direction. There was further evidence of discussion on the topic from the Fed minutes released last week.

- Potential drivers of higher for longer identified include:

- Permanently impaired global supply chains

- Changes in consumption and work patterns in the post-pandemic world

- Demographic shifts in major economies

- Increased borrowing needs of the US government

- Others in the camp expecting rates to settle back down bring up an important point: The economy always looks fine right before it sails off a cliff, and when it does, rates fall.

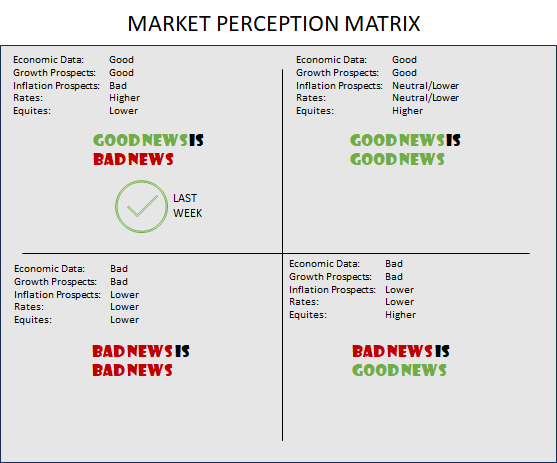

Deciphering the good news is bad news effect

- The Market Perception Matrix provides a simplified way of understanding the market schizophrenic reactions to economic data

- Last week was a good example of Good News Is Bad News when the S&P Global PMIs came in better than expected. On the same day, Initial Unemployment Claims came in lighter than expected, which also contributed to the perception that the economy has too much momentum for the Fed to ease soon and rates may remain higher for longer.

- One of the central problems with the Market Perception Matrix is that it is reactionary, focusing on just the most recent data release without context, and without looking at the larger picture and incorporating that into a forecast.

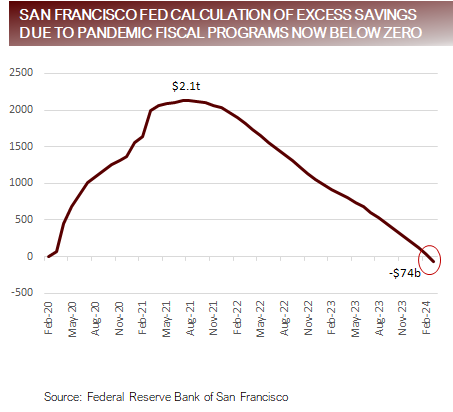

- In the larger picture, the labor market is showing signs of weakness and excess government sponsored pandemic savings have been extinguished, putting the markets at a potential inflection point for demand.

Labor market and savings normalized, setting the state for inflection point in demand

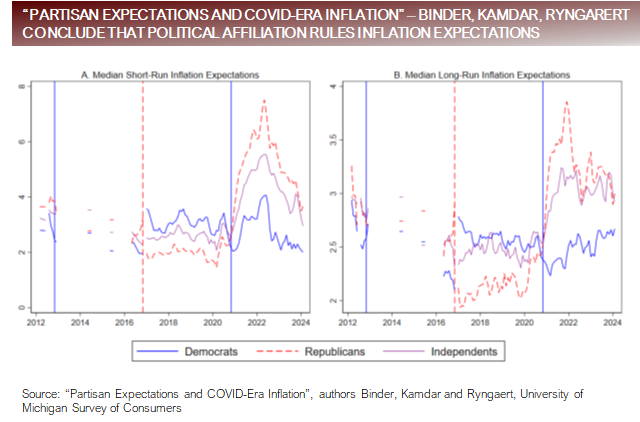

Inflation expectations, inflation and political affiliations

- In a recently published paper titled “Partisan Expectations and COVID-Era Inflation”, authors Binder, Kamdar and Ryngaert conclude that political affiliations had a strong relationship with perceptions of inflation since the pandemic, showing the Democrats have had inflation expectations relatively anchored, while Republicans and Independents expectations have become unhinged.

- Republicans

- Short-Run Inflation Expectations 4% to 7%

- Long-Run Inflation Expectations 3% to 4%

- Democrats

- Short-Run Inflation Expectations 3% to 4%

- Long-Run Inflation Expectations 25% to 2.75%

- Republicans

https://conference.nber.org/conf_papers/f192768.pdf

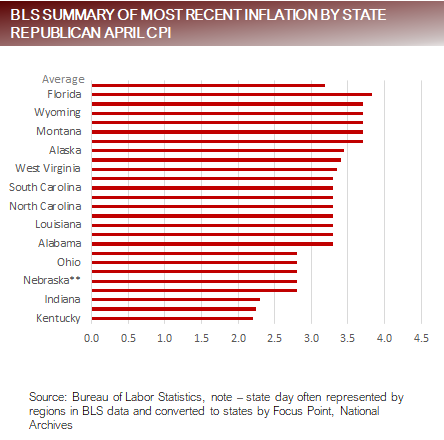

- We compared this analysis to the most recent data available from the Bureau of Labor Statistics and Bureau of Economic Analysis, analyzed by the states where Biden won the states were Trump won in 2020 as well as battleground states. Our analysis indicates the opposite of expectations.

- Republican States

- Average CPI (April) 2%

- Average Unemployment (April) 3%

- Average GDP Q42023 5%

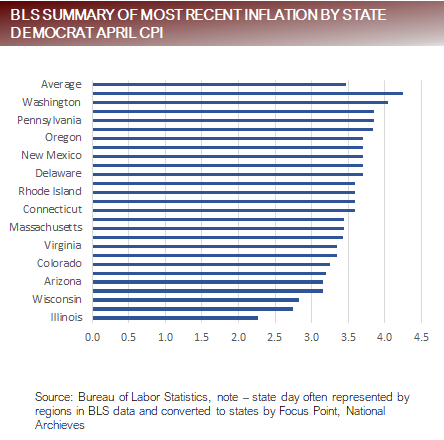

- Democrat States

- Average CPI (April) 5%

- Average Unemployment (April) 7%

- Average GDP Q42023 2%

- Republican States

Source: Bureau of Labor Statistics, note – state day often represented by regions in BLS data and converted to states by Focus Point, Bureau of Economic Analysis, National Archives

Research highlights how people from different political parties perceive inflation

Source: “Partisan Expectations and COVID-Era Inflation”, authors Binder, Kamdar and Ryngaert, University of Michigan Survey of Consumers

Focus Point research indicates the opposite of perceptions is true

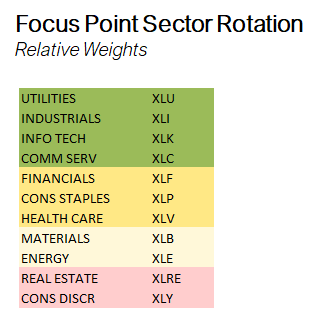

Sector Rotation Update: Market pressure shakes off weak trends

- The Focus Point Sector Rotation Model is a combined trend following and mean reversion model that utilizes seven factors to analyze daily price data on sectors to determine the strength of upward trends.

- The selloff last week shook loose the weak trends, with the model moving from 9 sectors with up trends to 4 sectors with up trends.

- Weakness deepened, with 2 sectors entering negative These are the 2 sectors we have been highlighting may be encountering fundamental areas of weakness.

- Real Estate: Fundamental weakness due to rising inventory, lower closing transactions and falling listing prices.

- Consumer Discretionary. Fundamental weakness due to slumping Retail Sales that may be associated with a softening the labor markets and exhaustion of government sponsored pandemic savings.

Putting it all together

- In last week’s commentary, for the first time this year we used the word “complacency”. The VIX Index had an 11 handle two days last week for the first time since 2019.

- Three recent surveys supporting the onset of complacency in investor attitudes:

- Bloomberg poll that indicated that only 23% of market participants are worried about a recession

- Bloomberg survey of economists indicating that they view the odds of a recession at 30%

- Conference Board Measure of CEO Confidence indicating that CEOs are the most confident they have been since 2019

- This reminds me of an old saying – when everyone is thinking the same thing, someone isn’t thinking.

- The New York Fed’s Global Supply Chain Pressure Index normalized to pre-pandemics trends in the middle of 2023, indicating that the supply pressures that had plagued the markets since the pandemic had largely been That was a key turning point, when the baton for the economy was handed from supply to demand.

- We’ll now see how far demand can take the baton after pandemic savings have run out and the labor market is showing signs of tarnishing.

- Based on coincident indicators, the economy is still performing very well, and risk assets will likely stand to benefit, but investors need to be vigilant for signs to not overstay their welcome in risk assets if the current begin to shift.

For more news, information, and strategy, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.