By Nicolas Fonseca, CFA, Product Manager

Fallen angels (as represented by the ICE US Fallen Angel High Yield 10% Constrained Index, “H0CF”) underperformed the broad high yield market (as represented by the ICE BofA US High Yield Index, “H0A0”) in October by 0.29% (-0.84% vs -0.55%), driven mostly by the rise in rates throughout the month, increasing the YTD underperformance to 2.14% (5.30% vs 7.44%). The 10Y Treasury yield jumped 47bps to 4.28%, a level not seen since July, as the market continued to recalibrate its expectations on the direction of interest rates. The wait for new fallen angels continues as Boeing raised equity and was able to end its labor strike, potentially providing some breathing room for the company. Moody’s confirmed Paramount’s Baa3 rating with a negative outlook, and. S&P Ratings has set its focus for new fallen angels on the commercial real estate sector, despite new back to office mandates and the U.S. Federal Reserve (Fed) easing cycle.

Rates Dominated as Spreads Tightened

In October, fallen angel and broad high-yield spreads tightened significantly, with high-yield spreads falling below 300 basis points for the first time since the global financial crisis (GFC). This tightening reflects strong economic fundamentals, robust credit conditions, ample liquidity and strong demand from yield-focused investors. Since October month-end, the higher rate/tighter spread trend accelerated following the U.S. election, likely reflecting adjusted forecasts for both growth and inflation.

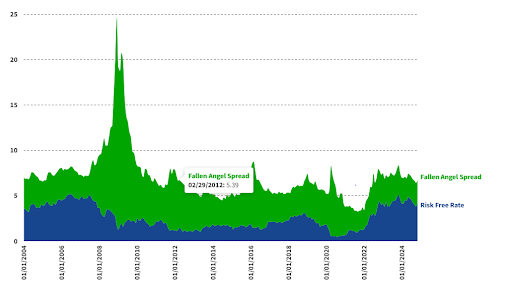

Historically, fallen angel spreads have played a key role in overall yields, especially when rates were low following the GFC. However, post-COVID rate hikes aimed at controlling inflation brought rates back as a primary driver of returns, reducing the relative contribution of spreads. Generally speaking, spread makes up a smaller portion of yields when the rates are higher as seen on the below chart. With the Fed expected to continue to cut rates through 2025 in response to a stabilizing labor market, spreads may take the driver seat again. As spreads become more influential, especially if rates decline in a spread-widening environment, we anticipate higher quality bonds to outperform lower quality ones.

Rates Make Up Greater Portion of Yields

Source: ICE Data Services, VanEck. Past performance is not indicative of future results.

Fallen Angels Overall Statistics: Fallen angel spreads tightened to 245bps, 14bps above their YTD low, however, broad high yield reached their tightest level since the post-financial crisis era (ending the month at 288bps) as yields rose due to a stronger economy and the possibility that the Fed may take a more gradual approach to rate cuts. Fallen angels and broad high yield average yields increased by 34 and 35bps, respectively, while the 10Y surged by 47bps to 4.28%, a level not seen since July as the market continues to recalibrate its expectations on growth and inflation. With rates rising, bond prices retreated in October, with fallen angels seeing a larger decline due to its longer maturity.

| Fallen Angels | Broad HY | |||||||||

| 12/31/2023 | 3/31/2024 | 6/30/2024 | 9/30/2024 | 10/31/2024 | 12/31/2023 | 3/31/2024 | 6/30/2024 | 9/30/2024 | 10/31/2024 | |

| Yield to Worst | 6.99 | 6.92 | 7.10 | 6.43 | 6.77 | 7.69 | 7.75 | 7.94 | 6.98 | 7.33 |

| Par Weighted Price | 91.20 | 91.22 | 90.32 | 93.69 | 92.31 | 91.86 | 93.18 | 92.98 | 96.72 | 95.72 |

| Effective Duration | 5.41 | 5.32 | 5.08 | 5.04 | 5.04 | 3.31 | 3.28 | 3.26 | 3.04 | 3.19 |

| Full Market Value ($mn) | 67,821 | 64,657 | 55,371 | 57,236 | 55,362 | 1,237,721 | 1,260,542 | 1,266,993 | 1,336,160 | 1,328,101 |

| OAS | 285 | 247 | 252 | 261 | 245 | 339 | 315 | 321 | 303 | 288 |

| No. of Issues | 143 | 138 | 126 | 124 | 122 | 1,837 | 1,864 | 1,863 | 1,873 | 1,875 |

Source: ICE Data Services, VanEck. Fallen Angels: ICE US Fallen Angel High Yield 10% Constrained Index. Broad HY: ICE BofA US High Yield Index. OAS refers to “option-adjusted spread.” Please see definition for this and other terms referenced herein in the disclosures and definitions portion of this blog. Past performance is no guarantee of future results. Index performance is not representative of strategy performance. It is not possible to invest in an index.

Fallen Angels: There were no new fallen angels in October. Boeing, a potential fallen angel, had the largest stock sale by a U.S. company as it tried to repair its balance sheet to avoid a downgrade to high yield. Overall, the credit rating agencies were supportive of the equity raise and the end of its labor strike, alleviating some of the downgrade risk, although Boeing is still not completely out of the woods just yet. More broadly, Barclays estimates between $40bn to $60bn of new fallen angels in 2025 as interest rates remain high with big names such as Paramount, Warner Bros and Charter Communications at elevated risk of becoming fallen angels.

| Month-end Addition | Name | Rating | Sector | Industry | % Mkt Value | Price |

| January | Hudson Pacific Properties LP | BB1 | Real Estate | REITs | 2.18 | 88.05 |

| February | Advance Auto Parts Inc. | BB1 | Retail | Specialty Retail | 2.52 | 91.20 |

| September | OCI NV | BB1 | Basic Industry | Chemicals | 1.10 | 104.79 |

| September | V.F. Corp | BB1 | Retail | Specialty Retail | 3.04 | 94.08 |

Source: ICE Data Services, VanEck. Fallen Angels: ICE US Fallen Angel High Yield 10% Constrained Index. Past performance is no guarantee of future results. Not a recommendation to buy or sell any of the names/securities mentioned herein. Index performance is not representative of strategy performance. It is not possible to invest in an index.

Rising Stars: No risings stars in October.

| Month-end Exit | Name | Rating | Sector | Industry | % Mkt Value | Price |

| February | Las Vegas Sands Corp | BB1 | Leisure | Gaming | 3.12 | 93.19 |

| March | Enlink Midstream Partners LP | BB1 | Energy | Gas Distribution | 2.30 | 88.92 |

| April | FirstEnergy Corp. | BB1 | Utility | Electric-Integrated | 6.62 | 87.10 |

| April | Rolls-Royce PLC | BB1 | Capital Goods | Aerospace/Defense | 1.51 | 96.00 |

| July | Delta Air Lines Inc. | BB1 | Transportation | Air Transportation | 1.50 | 94.59 |

| September | Port of Newcastle Investments Financing Pty Limited | BB1 | Transportation | Transport Infrastructure/Services | 0.52 | 95.59 |

Source: ICE Data Services, VanEck. Fallen Angels: ICE US Fallen Angel High Yield 10% Constrained Index. Past performance is no guarantee of future results. Not a recommendation to buy or sell any of the names/securities mentioned herein. Index performance is not representative of strategy performance. It is not possible to invest in an index.

Fallen Angels Performance by Sector: The Healthcare and Leisure sectors decreased their exposure in the Index as one issuer was removed from each sector (an issuer didn’t meet the index requirements; the other’s bond was redeemed). Only Banking and Consumer Goods posted positive returns in October, driven by spread tightening in the Banking sector and spread tightening and price appreciating in the Consumer Goods sector. Regarding sector attribution vs a broad high yield, Consumer Goods was the main contributor while Tech was the main detractor. Within Consumer Goods, the fallen angel index only holds Newell Brands bonds which outperformed the +40 issuers in the broad high yield market. In Tech, Xerox was the main culprit.

| Wgt (%) | OAS | Price | Total Return | ||||||||||

| 12/31/23 | 6/30/24 | 9/30/24 | 10/31/24 | 12/31/23 | 6/30/24 | 9/30/24 | 10/31/24 | 12/31/23 | 6/30/24 | 9/30/24 | 10/31/24 | MTD | |

| Banking | 4.79 | 5.38 | 5.45 | 5.64 | 231 | 220 | 210 | 181 | 97.91 | 97.36 | 101.29 | 101.12 | 0.30 |

| Basic Industry | 1.70 | 3.73 | 4.78 | 4.85 | 171 | 156 | 190 | 184 | 97.24 | 95.03 | 99.25 | 96.84 | -1.99 |

| Capital Goods | 5.85 | 5.41 | 5.31 | 5.43 | 200 | 161 | 198 | 172 | 97.34 | 97.51 | 98.72 | 97.75 | -0.50 |

| Consumer Goods | 4.33 | 5.28 | 5.22 | 5.49 | 230 | 240 | 231 | 174 | 94.29 | 93.64 | 97.25 | 98.52 | 1.83 |

| Energy | 14.75 | 12.27 | 12.13 | 12.35 | 259 | 239 | 267 | 249 | 92.49 | 93.44 | 95.40 | 94.02 | -0.93 |

| Financial Services | 1.14 | 1.37 | 1.40 | 1.43 | 378 | 376 | 324 | 301 | 86.41 | 84.87 | 91.57 | 89.95 | -1.27 |

| Healthcare | 4.10 | 5.15 | 5.29 | 4.10 | 270 | 207 | 157 | 198 | 88.73 | 91.12 | 95.88 | 91.85 | -1.88 |

| Insurance | 1.32 | 1.65 | 1.67 | 1.68 | 323 | 238 | 237 | 218 | 94.10 | 96.11 | 100.34 | 98.44 | -1.31 |

| Leisure | 7.90 | 5.92 | 4.90 | 4.31 | 228 | 180 | 234 | 238 | 93.21 | 94.48 | 95.41 | 93.18 | -0.91 |

| Real Estate | 9.07 | 10.07 | 10.23 | 10.42 | 675 | 450 | 389 | 404 | 82.72 | 84.76 | 89.79 | 88.24 | -1.30 |

| Retail | 14.38 | 20.45 | 21.67 | 22.13 | 242 | 196 | 252 | 222 | 86.39 | 88.19 | 88.38 | 87.51 | -0.58 |

| Services | 0.64 | 0.79 | 0.78 | 0.80 | 243 | 206 | 202 | 193 | 94.78 | 94.67 | 98.11 | 96.36 | -1.34 |

| Technology & Electronics | 6.22 | 6.67 | 6.66 | 6.64 | 194 | 184 | 206 | 203 | 94.14 | 92.27 | 94.38 | 91.54 | -2.53 |

| Telecommunications | 13.00 | 11.10 | 11.82 | 12.01 | 366 | 413 | 351 | 324 | 92.22 | 81.48 | 92.33 | 91.12 | -0.68 |

| Transportation | 2.09 | 2.60 | 0.57 | 0.57 | 209 | 150 | 210 | 178 | 94.92 | 96.07 | 106.22 | 104.75 | -0.83 |

| Utility | 8.71 | 2.17 | 2.11 | 2.16 | 139 | 185 | 203 | 166 | 92.18 | 96.23 | 99.44 | 98.53 | -0.46 |

| Total | 100 | 100 | 100 | 100 | 285 | 252 | 261 | 245 | 91.20 | 90.32 | 93.69 | 92.31 | -0.84 |

Source: ICE Data Services, VanEck. Returns are based on partial period data. Fallen Angels: ICE US Fallen Angel High Yield 10% Constrained Index. Not intended as a recommendation to invest or divest in any of the sectors mentioned herein. Index performance is not representative of strategy performance. It is not possible to invest in an index.

Fallen Angels Performance by Rating: There were no changes in the fallen angels rating allocation for October, with BB-rated fallen angels still dominating the Index. CCC rated fallen angels outperformed higher- and lower-rated peers as their spreads tightened by more than 10% to 417bps, reaching their post GFC low in October, and seeing their price increase as yields were relatively unchanged. Relative to the broad high yield market, the fallen angel underperformance was primarily from the spread effects of the BB-rated issuers.

| Wgt (%) | OAS | Price | Total Return | ||||||||||

| 12/31/23 | 6/30/24 | 9/30/24 | 10/31/24 | 12/31/23 | 6/30/24 | 9/30/24 | 10/31/24 | 12/31/23 | 6/30/24 | 9/30/24 | 10/31/24 | MTD | |

| BB | 80.55 | 87.62 | 87.30 | 87.03 | 219 | 210 | 223 | 207 | 92.44 | 92.62 | 95.29 | 93.91 | -0.85 |

| B | 13.43 | 7.89 | 7.32 | 7.39 | 317 | 371 | 382 | 385 | 96.46 | 90.73 | 92.36 | 90.22 | -1.79 |

| CCC | 5.44 | 4.19 | 4.38 | 4.56 | 1,130 | 505 | 468 | 417 | 69.40 | 80.90 | 87.61 | 88.32 | 1.37 |

| CC* | 0.30 | 1.00 | 1.01 | 5,719 | 1,703 | 1,734 | 13.00 | 44.51 | 42.82 | -2.17 | |||

| Total | 100 | 100 | 100 | 100.00 | 285 | 252 | 261 | 245 | 91.20 | 90.32 | 93.69 | 92.31 | -0.84 |

Source: ICE Data Services, VanEck. Fallen Angels: ICE US Fallen Angel High Yield 10% Constrained Index. Not intended as a recommendation to invest or divest in any of the sectors mentioned herein. Index performance is not representative of strategy performance. It is not possible to invest in an index. BB index: ICE BofA BB US High Yield Index; Single-B index: ICE BofA Single-B US High Yield Index; CCC & Lower rated index ICE BofA CCC & Lower US High Yield Index. *Doesn’t have securities for all months of selective periods. Returns are based on partial period data.

To receive more Income Investing insights, sign up in our subscription center.

Originally published 14 November 2024.

For more news, information, and analysis, visit the Beyond Basic Beta Channel.